Category Archives: Advisers

Marketlend Academy: How much should a small business spend on marketing?

Selling yourself is a part of every business, and marketing is the way it’s done at scale. But how much should a small business spend on marketing?

Like any question worth asking, the answer depends on your situation. Read on for some insight into what businesses are spending on marketing today, and what you need to think about before setting your own marketing spend.

Define your needs

What you want to achieve goes a long way to determining your budget. Your needs are different from other companies and will change over time. You may want to:

– Grow fast

– Grow sustainably

– Build brand awareness

– Maintain an established presence

These are all very different goals, with different associated costs. If you’re just starting out, every company needs a cohesive brand and a functional, professional website. Beyond that, your needs are completely custom.

With that caveat, there are some standards you can use to set your expectations.

How much should a small business spend on marketing?

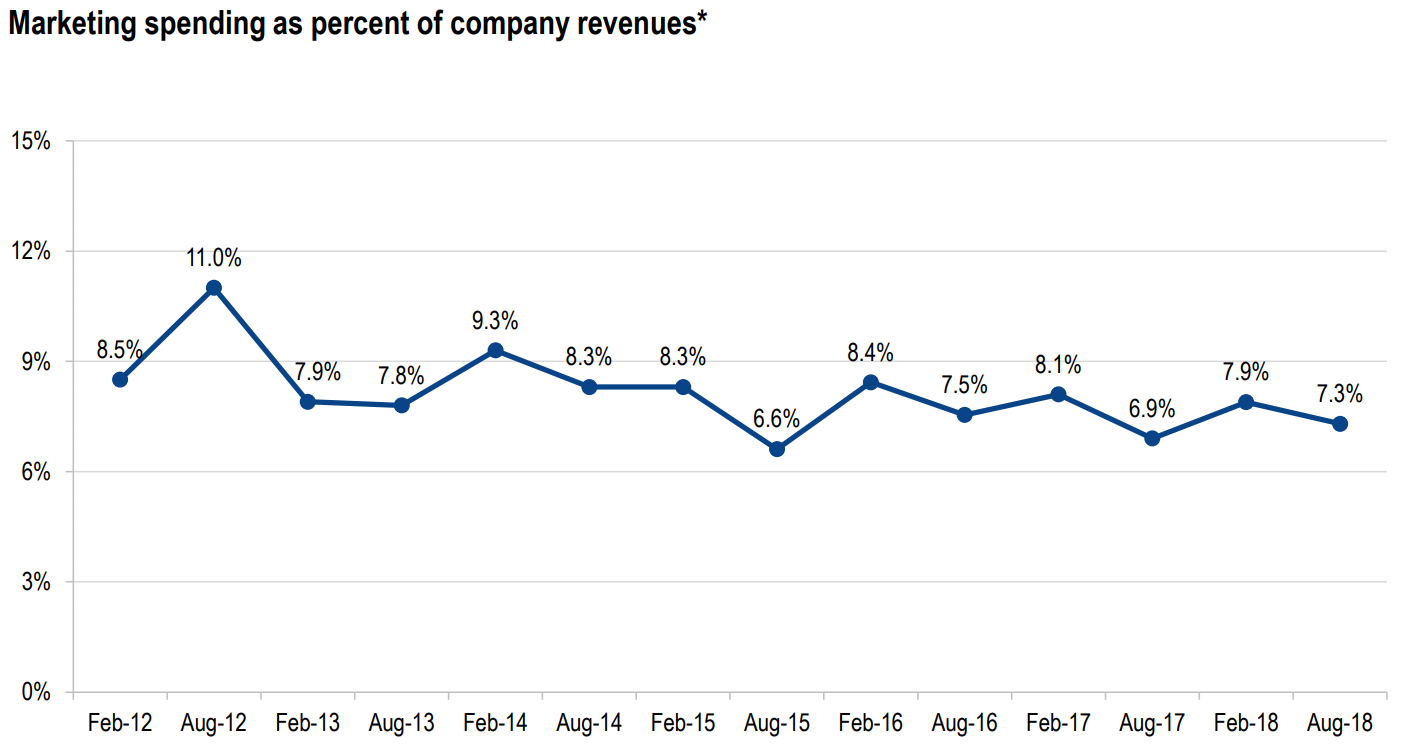

Marketing budgets are normally measured as a percent of company revenues. To get a dollar amount from the percentages below, multiple them by a firm’s gross revenue.

The August 2018 CMO Survey from the American Marketing Association found an average marketing spend of 7.3% of company revenues from 324 respondents across the US.

The chart below shows this is lower than recent years, but still within a typical range of 7-9% of revenue (source page 26).

Marketing for startups vs established firms

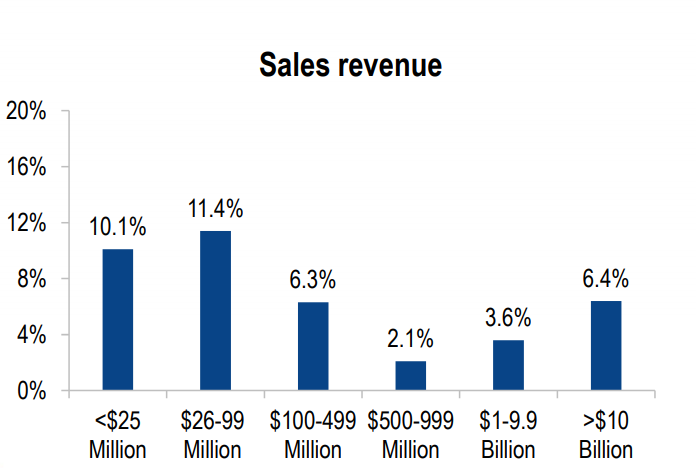

The report calculated average marketing spend by company size, as seen below (source page 27). Generally, smaller firms spend more on marketing than larger companies.

The first step of marketing is brand awareness, so smaller businesses without established brands are wise to spend more on marketing. Established brands can get away with a more efficient budget.

Ryan Flannagan of Nuance Media writes startups should expect to spend 12-20% of gross revenue on marketing, while noting a larger firm may only spend 6-12% of gross revenue on their marketing budget.

When the rules don’t apply

Knowing the rules helps you know when to ignore them, and a standard marketing budget won’t suit every company.

The CMO Survey breaks down marketing budgets as a percent of firm revenues by sector, below (source page 27).

Clearly there are situations where a big traditional marketing spend isn’t as useful. B2B services like mining, manufacturing, and professional services for instance typically rely on sales teams to attract new clients (with sales rarely included in marketing budgets).

Avoiding over-marketing

You can over-spend on marketing. First, there’s the opportunity cost of a high marketing budget that may be better spent on product or business development.

But there’s also the risk of growing too fast. If your marketing is too effective, you may face more growth than you can handle. That can cause serious cash flow problems that undermine other parts of your business, potentially sending you out of business.

Avoiding this isn’t difficult. First, don’t borrow more than what you need for the growth you can handle. If you’re using Marketlend to access flexible, peer-to-peer finance, don’t over leverage yourself. Make your repayments and you can always extend your line of credit later.

If you do have cash flow issues as you grow, a service like UnLock can provide extended payment terms to supercharge your cash flow, like a corporate version of buy-now-pay-later.

Pay it smart

The key element when setting a marketing budget is to be deliberate. Approach your marketing spend with a critical mind and a clear vision of what you want to achieve, and you’ll be miles ahead of the competition already.

Inadequate regulation of fintech leaves Australian SMEs at risk

By all accounts, Australia is poised to become one of the world leaders in fintech. We’re an incubator for new ideas and experimentation. Despite this, an inadequate regulatory environment and lack of support for small-to-medium enterprises (SMEs) continues to put the fintech industry, and the small business community, at unnecessary risk.

The stakes for Australia’s economy are high. Small businesses, which employ half of the nation’s workforce and make one fifth of its domestic product, remain vulnerable to the loan shark practices of fintech bad guys.

That’s true even with a new voluntary code of lending practice that Fintech Australia recently put in place to self-police albeit not all lenders are even members of the organisation. The code claims to standardise transparency and create a mechanism to resolve disputes, but only six fintech companies have signed on and it has no real teeth.

While the code includes a pledge to lend only to SMEs that have the capacity to repay, there is no mechanism to stop loans to SMEs that have outstanding loans from other fintechs — a practice known as “stacking.” Nor does the code address some lenders’ insistence on repayment by relentless direct debits that can drive SMEs out of business. Finally, it’s not clear whether the code can be enforced or is merely a set of guidelines.

In other words, we’re not signing up because it is not a legitimate attempt to enable responsible lending — it’s an empty gesture for a quick PR hit. As mentioned it does not apply to non-Fintech Australia members. Furthermore, its definition of an SME loan excludes the majority of the lending in the SME arena.

In effect, then, the problems that brought on the code still exist. As an experienced SME lender, we are gobsmacked how anyone can suggest that the majority of SMEs will understand the real cost when a loan is offered on a factor rate (shouldn’t it be as simple as the question, what is the interest rate after all costs?). In fact, reports of ASIC’s recently completed review of one of the most prominent fintech SME lenders are notable for absenting lender’s factor rates from review and thus excluding what is arguably the most problematic and damaging part for SMEs from scrutiny.

While fintechs can still serve startups as an excellent alternative to traditional banks, particularly if they’re small- or medium-sized, some startups will likely still fall prey to unscrupulous practices. We have seen SMEs who have had their cash flow drained by frequent debits they could not afford and literally have to close up shop, and, even more unbelievably, it was accountants and other financial advisors who recommended these kinds of loans for their unsuspecting clients.

So the regulatory environment needs to be strengthened, and Australia needs to provide more education and better support for small businesses. The reality is, it’s easier to start a new business in Australia than it is to get a driver’s license, and that’s not a good thing.

There’s a big difference between having a good business idea, and having the business acumen to get it off the ground. More than half of SMEs close within the first three years, and the most common reason is financial hardship.

There are some simple steps that the government could take to address these problems. It could apply the National Credit Code for Retail to SMEs, so they would come under its protections, at least for loans under A$100,000. These include a bar on extending credit to consumers who are likely to have difficulty making payments. Further, the code of lending practice should be amended to forbid loan stacking and mandatory debits. It could remove prepayment penalties, why should an SME suffer to paying a loan out early. Isn’t this a sign of a well run business?

The government should also support SMEs with a licensing and education. With such a program, new entrepreneurs could have a better understanding of money, marketing, cash flow and lending — including the ability to spot a bad loan a mile off.

Why is this so crucial?

It’s crucial because SMEs serve as the economy’s engine. If too many SMEs go belly up from poor business decisions, including bad loans from shady fintech lenders, it affects a fundamental base of our economy and it hurts Australia’s reputation as a fintech innovator.

Our fintech industry now ranks among the top ten in the world. If we pay attention to the small businesses upon which it is built, Australia can further strengthen its reputation. Everybody wins: The SMEs, which will be less likely to go out of business; the lenders, who will be less likely to lose money on bad risks; and the nation, which will continue to thrive as a world leader in fintech.

Marketlend Academy: what makes Marketlend unique?

Founder and CEO of Marketlend Leo Tyndall explains the significant differences that make the Marketlend platform so powerful and supportive for investors. If you prefer, you can read the transcript below.

What makes Marketlend unique is that we’re able to give SMEs direct access to the capital markets, but in a secure and also price competitive environment. By using insurance, and also using loss reserves, we’re able to give the SME the benefit of those so therefore getting better pricing for them, and at the same time give the investor comfort that when they invest in an SME, that they have additional protection against the possibility of a loss. Now, matching … In, in, by doing this we use trade credit facilities, which is an unusual thing. In that, what we’re doing is, we’re becoming the owner of the goods. And then essentially what we’re finding is the SME’s able to then buy more goods and then within 90 days repay us, and therefore giving them an improved profitability so that they have a, a better, you know, cost of funds. And then also, giving them the ability to have money now versus waiting for 30, 60, 90 days depending on the type of facility. So it’s actually having the money to actually pay expenses or buy more goods and enable them to improve their profitability of their business.

Marketlend Academy: what we look for in investors

Watch Marketlend’s Chief Investment Officer, Jane Lehmann, talk about what Marketlend looks for in its investors. The text of her comments appears below if you prefer to read.

Marketlend has a very specific requirement in regards to its investors. Under the Corporations Act, we are required to only engage experienced, sophisticated, wholesale, official investors. So for an experienced investor, that really is someone who can demonstrate that they have, as the name suggests, experience in lending in these types of financial instruments, and truly understand the risks that they’re undertaking when they engage in the platform. Sophisticated is actually a means test related defining feature that you need assets of a 2.5 million. I think the inference there is they also are a more sophisticated and experienced investor.

The institutional investors have a different profile that they tend to be funds. Many of them are offshore. And for them they often have a specific risk profile that they’re interested in and we can customise that for them. We have a pool of loans that we have onboarded and we can work with them to understand what their risk tolerance is where there are risk sectors they’re not comfortable with, where they have an appetite and craft a portfolio for them.

The experienced and sophisticated investors have the opportunity to go on to the platform and make their own assessments. They can look at each loan that is presented and make their own assessment and take a view on whether that is something that appeals to them as an investment opportunity. And that is obviously why you need experienced investors, because they are making a financial decision.

Marketlend Academy: Does your SME need a branding consultant?

Branding, where does it fit? Determining which job functions to prioritise in an SME is one of the most critical resource decisions you’ll make as a founder. The need to focus foremost on services and product development is obvious, but business experts often debate the merits of investing in strong branding.

It’s not necessarily a key factor in whether an investor may choose to fund your business, but it’s important to make a good impression. So how much money should you actually spend and who should you work with to build a reasonable branding plan? Consider some of the following factors to help you decide what’s best for your business.

What is your branding IQ?

If your idea of branding means paying a random designer $10 on Fiverr to create your logo, you might be underestimating some things. (That’s not to say this approach doesn’t magically work out well sometimes! Best of luck to you.) Get real with yourself about how much of a priority branding needs to be in your business. Plan to invest some time. In fact, let’s pause for a moment. Complete outsourcing is not really possible when it comes to branding. This business is your passion and even the best consultant will need you to set aside a few hours a week to collaborate and extract authentic representations of your work from you. The absolute worst thing you could do is throw money at someone and expect a brand to materialize without nurturing on your end.

How much can you expect out of your branding consultant?

At a bare minimum, a decent branding plan should involve 10-15 hours of work with a trusted professional who will create a roadmap for success. Advanced branding should be an integrated component of your overall marketing strategy. In the social media era, this usually includes a supplemental content strategy for which you would create assets like written blog content, graphics, photos, podcasts or videos. You’d also want to create a system for deploying this branded content to firmly-defined key audiences. A top-notch branding consultant should be able to help you conceptualize your aesthetic, your content and deployment strategy, and connect these efforts back to your sales funnel.

Where can you find them?

As you begin your search, consider the merits of working with an agency versus a freelance individual. Intangibles, such as personal compatibility and working styles, are also important. Agencies offer more brain power and hands on deck; the access to a broader infrastructure can lead to increased operational smoothness and responsiveness.They are also more expensive than individuals, who often leave agencies to enjoy the benefits of self-employment. Be open-minded. Branding consultants are usually creatives who embrace flexibility. Just be wary of anyone who presents themselves as a one-stop shop of expertise. Ask an individual who else they plan to work with on design and production, and find out if there are hidden or unanticipated costs for ancillary things like social media advertising budget on top of their fees.

The best bet is to ask colleagues for recommendations. You can also try LinkedIn searches. Sites like CloudPeeps, Dribbble, Carbonmade, and Thumbtack can also be a good bet. You may also want to research private Facebook groups for freelance creative professionals and see if you can post your job description.

How much should you invest?

Your budget will be a major factor in how things go with your branding consultant.

There are awesome, enterprising young people who are building up their portfolios willing to work for as low as $25-50/hour. A mid-career professional can run about $75/hour. Heavy-hitters will ask for $150+ hourly rates. Any of these folks might be willing to negotiate a flat rate deal with you as well. Agencies typically charge a monthly retainer from $2,500 to $10,000. Be willing to suggest a startup discount, services trade, or payment installment plan if it would allow you to work with someone you’re excited about. They might say yes!

How long should you work together?

The duration of your agreement is heavily dependent on your initial goals. A top-level evaluation from a major strategist could take a week. A first iteration and basic roadmap could be completed in 4-6 weeks. A more advanced engagement could last 3-6 months. Whatever you decide in coordination with your branding consultant, be sure to build a mid-point check in to ensure you’re on track to hit your agreed upon deliverables.

Marketlend Academy: Marketing Your SME

Let’s say you’ve come up with a cure for baldness. You’ve patented your formula, written a business plan, lined up investors, hired staff and set up production. Ready for liftoff, right? Nope. Your startup would crash for want of marketing.

You can’t sell something, even the cure for baldness, unless people know it exists. Lots of people. Marketing is how you let them know your product exists, and also how you make it appealing. Product design, consumer research and advertising all come under marketing’s umbrella. Pricing strategy–or at least, the case you make to the consumer that the price is right–comes under marketing, too.

The elements are many, and your business needs an approach that incorporates some or all of them. The best strategy for any given business usually includes a mix. For example, logo development, media outreach, paid advertising and trade shows. Here are tips for deciding what marketing strategies might work for your startup and ways to get started.

Fine-tune your marketing plan

Ideally, your business plan addressed marketing to some degree, but you’ll want to flesh this out in a plan exclusively focused on marketing before you go live. You’ll want it to start with an explanation of why your product is better than your competitors’ and accurately describe your niche.This is called the “situational analysis.”

Add on a short description of your ideal prospective customer and their earnings, gender, age, family composition and consumer habits. Also Include the type of media this hypothetical person likes to consume–internet, newspapers, television, radio, podcasts, etc.. A person over 65, for example, is less likely to use Instagram than a person in their early 20s. This section will require you to do a bit of research, but it will bear fruit.

Next, list some very specific, measurable goals you want to reach, such as a 10 percent increase in sales in your second year of operations. You want your goals to be measurable so you’ll know if you reached them.

And of course, you need to list your tactics for spreading the word about your product so that it reaches prospective customers. Take into account the different stage of the sales cycle and determine how you plan to reach cold prospects and how you want to reach existing customers, whether its through radio advertising or loyalty programs. Options are many, from banner ads online to banners pulled by planes; from chatty blogs to the sparse wording on a billboard.

Set your marketing budget

Be prepared: marketing can be costly. Most startups decide on a marketing budget that’s a percentage of their projected revenue. But the recommended ratio varies by industry, so it would be wise to seek advice from your industry’s trade association.

Some companies spend up to half of their sales revenue on marketing in their first year and 30 percent of that revenue thereafter. One school of thought holds that companies in their first five years of business should allocate 12 to 20 percent of their gross or projected revenue for marketing every year while older companies should allocate up to 10 percent. One tool that might be helpful is the National Australia Bank’s marketing budget forecast template.

Measure your results

Unless you measure the results of your marketing efforts, it’s hardly worth drawing up a plan in the first place. Measurement helps you fine-tune your tactics so they’re better at reaching your intended audience. It lets you know when an approach isn’t working so you can regroup and try something else. Your metrics will hinge on your tactics. Print advertising could direct people to a designated phone number or internet domain and you could count how many calls or views it gets. Online promotions and clicks can be measured using internet analytics. If you use billboard advertising, the billboard company will have a way to measure the number of cars and pedestrians who walk past every day.

Planning backed up by careful research; budgeting that’s realistic; and measuring that tracks results are cornerstones of effective marketing. If you market your product well, potential customers will recognize your brand, distinguish it from your competitors and favor it.

Marketlend Academy: How are your loans different from other SME lines of credit?

Lending to SMEs to support sustainable growth is what Marketlend CEO and Founder Leo Tyndall is passionate about, and he wants his company to lead the way as a responsible organisation that treats lines of credit with care and delivers transparency. Click to video to here more or scroll down for a transcript of his latest chat.

So when you say giving them a line of credit, and pay them straight, no, we don’t, we pay their suppliers. So, we pay their suppliers, and we pay their suppliers based on invoice of the verified and checked, and those invoices are then presented to us, and then we pay that supplier, and then when they actually get the goods, they then sell them, and obviously then they pay us in the 90 days after that.

So, and even if our line of credit, uninsured which is a product, which is a little bit similar to like a loan, but it’s a limit, we pay the supplier. So, we allow them to pay suppliers, or services, and what we provide is a line of credit. It’s a little bit similar to an overdraft: we give them a line of credit, it’s renewable, and reviewable every 12 months, they pay it on time, investors are happy, now roll the facility over, and they can keep it going. And, the point being, is that they can then run their business knowing that if they get a big order, they’ve got this line of credit they can use, if they don’t have many orders, they can close the line down, or can reduce it, so there’s that flexibility there.

And that’s not what they’ve got when they go and get personal loans, or I call them personal loans, but S and E loans, ’cause they’re just pure loans.

Yeah, correct. yeah, and the other reason why we do that, is that we don’t really like the idea of giving people pure cash, because it could be used for alcoholism, gambling, and a few other, we’ve seen one before, where they present an invoice and we went to pay it, but before we paid the invoice, we looked at these bank statements and noticed that he was actually gambling. So, we said, “Look, we don’t think we’re gonna pay that.” Because, obviously, we look at their bank statements, and he was probably gonna use the cash that we paid for the goods, with his own income so he could do some gambling or whatever he was gonna do.

So, we look at their bank statements, so we have a number of steps, so, first thing we do is we actually look at their ability to repay the debt for debt servicing ratios, and they’re financials, after their financials we give their bank statements, we then review their bank statements and look at the entries on the bank statement. We have a team member whose only job is to look at those bank statements, and what he’ll do is, he’s a risk officer, and he’ll identify any unusual activity, but also the ability to repay, because the financials may not match the bank statement as well.

And then in this case, what we did was we saw that there was a number of gambling sites that were being paid, and even though we weren’t providing him the cash, we identified that that was a risk, and we didn’t want to lend to him.

Marketlend Academy: How Can I Fund my Business?

Funding is often a constant concern for SMEs. To fund a business doesn’t just mean finance and there are creative ways to bring money in the door that can support growth.

What are your best options for funding? Here are some “outside-of-the-box” options that can help.

Presell Services or Products

This is a creative way to fundraise when your business is in the early stages. Get your elevator pitch ready for anyone who wants to talk about your new project. If you plan to offer a consulting service, web security, a new line of grocery stores, offer a presale.

A presale means you receive money before your grand opening. Give your customers proof of purchase, such as a coupon, to be redeemed when the business opens. Customers love to help a business they believe in and are happy to exchange a proof of purchase for something new.

This works best if you can show proof that your business is more than a concept. Blueprints for your new building, a working model, or an online store all help push presales.

Approach Angel Investors

If you have a tech startup or product idea that will disrupt a market, try pitching to a group of angel investors. If you get an offer of money, it will come with the caveat of equity. Angels want to take part in any business they fund, so they choose businesses they know well or like. This can work to your advantage if you are open to hearing a new voice as you build or expand. However, if you don’t want a board or individual looking over your shoulder or combing through your books, this might be a detriment to your growth.

The key to approaching angel investors is use your connections and your reputation. Start by asking people you already know if they have any connections to the investment community and use those familial or social ties to build your network. When you meet a new investor because a mutual, and trusted colleague introduced you, the prospect of getting money is much greater.

If no one can give you an introduction, try a cold email or a message sent without the buffer of a personal introduction first. Research the investor you want to talk to and see what kinds of projects they prefer. Stick to those who are active in your industry and go for it.

Once you take meetings, be sure to be as transparent as possible with your numbers. Any exaggeration or dishonesties will paint you in a negative hue and keep potential partners at bay. Be yourself and let your business speak for itself to win people over.

Crowdfund Online

Crowdfunding sites like Kickstarter let you set a financial goal, break down your vision and timeline for visitors, then market yourself to potential donors. Each campaign has a set number of days to raise the necessary money. If you reach your goal, you get the money deposited into your account and the site asks for a small percentage of what you earned. If the donations fall short, you receive nothing.

Successful campaigns start long before they are up on the crowdfunding site. This requires marketing videos, a large following and tons of buzz over what you have in the works. The most successful campaigns have money promised to them before the timer ticks down.

Once the campaign is up, it can be a full-time job to manage the social media and email marketing to bring in additional money. You will also have to organise rewards for donors that don’t gobble up all your new money but still make it worthwhile to give. A campaign requires creative marketing in all outlets in order to succeed.

It’s a lot to handle, but people make real money on these sites. If you are a master of marketing, this is a good option.

Government Grants

Australia’s government offers a variety of grants for small businesses, but expect a complex application process and very specific criteria for funding.

Grants are available at the state or federal level and are listed online. They tend to favor specific projects or a stage of business, such as funds to start or funds to hire as you expand. Research grants ahead of time so you know what to apply for throughout the year. Tailor each application to the specific grant, don’t rely on generic forms and answer each question with clear, honest responses.

Some of the categories for grants include expansion, green business or disaster recovery. They’ve been created to help solve problems as opposed to a basic round of funding. Check out the whole list and mark which ones line up with your business or future undertaking, then mark due dates on your calendar. If you can talk to someone who received a grant in the past, ask for advice on how to present your problem in the best way possible.

Before you Finance

Still think you may need finance? Here are some things to avoid to help you make finding finance smoother and more likely to lead to success:

- Not working with an accountant – Many business owners turn to bookkeepers, but an accountant will keep your statements in order and all your numbers on point.

- The wrong partner – Investors want to see dynamic teams that balance each other out and have a clear vision with a solid plan to put it in place. Don’t waste time with someone who is unprofessional or doubts your vision. Find a partner who shares your vision and knows exactly how to help you succeed.

- No plan for the money – Anyone who funds you wants to know your plan on how to spend it. Have all of that in place before you borrow or accept the grant.

- Waiting to ask – Plan out your search for finances early. The decision to put off the search for finances can put unnecessary stress on your business. You know what you need to stay functional, so don’t hesitate to ask for it

Marketlend Academy: A Chat With Chris Van Homrigh

As a former Regional Commissioner NSW, Australian Securities & Investment Commission, Chris Van Homrigh has brought his deep background in market regulation and best practice to the Marketlend team over the last year. At Marketlend, this knowledge and experience has helped support the continual refinement of a first-of-its-kind lending platform, and our constant focus on transparency and delivery of value for investors and SMEs. If you prefer to read Homrigh’s thoughts, you can scroll down for the transcript.

Well, I mean, if you look back at what ASIC looks at, it primarily has two primary objectives: one, is to have a fair and efficient markets, and the other is about having confident, informed consumers, and investors, or financial consumers, and investors. So, from a regulatory perspective, working on the investors’ side, it’s about knowing what we need to disclose to investors, the level of detail.

Marketlend, as you know, is quite transparent with all the information we provide. So, when we establish a facility with a borrower, all the information that we have, with respect to that borrower, is basically passed through to the investors. So, disclosure is a big tenant. Asset focuses a lot on disclosure, so it’s being consistent, and very apparent with the disclosure.

Again, being a lending business, there’s always loans that you don’t think are going to go into arrears, but they’ll go into arrears, or potentially go into default, and again, it’s about getting the information in a timely manner across to the investors, and the right level of information.

Now, of course we do have some investors who want more information than others, but, again, it’s about getting that information, and answering their questions. Sometimes with the legal process where things go into arrears or in default, that can be protracted. Investors are always concerned about getting their money back in a timely basis, and obviously in return they get for making the investments.

Martketlend Academy: 4 ways to improve your shot at getting business finance

Need some general tips on improving your small business’s health –especially when it comes to getting finance? This week, we have the pleasure of welcoming Bessie Hassan, who shares our drive to educate the market and help small businesses. As the Money Expert for finder.com.au – the site that compares virtually everything – Bessie is an experienced commentator who often appears on national radio, TV, and throughout online publications sharing her best money-saving tips and property advice. Bessie is passionate about empowering Australians to make better decisions, whatever it is they’re looking for.

Whether you’re an entrepreneur looking to start a new business from scratch or a seasoned owner wanting to expand your business offshore, you’re going to need some capital at some point. To get your hands on this extra dosh, it’s likely you’ll need to take out a business loan. In business, time is money and money is time, so it’s worth knowing a thing or two about how to apply for finance the right way.

Here are four ways to improve your chance of getting the “green light” for your business loan.

1. Check your credit health

Although we’re told to keep our business and personal lives separate, this rarely happens for business owners, as lenders often look at both your company and personal credit scores before lending you money. There’s no point applying for a business loan if you know you don’t have a great credit history (either personally or via your business). Being patient and working to improve your credit score before applying will give you a better chance of securing finance.

Your company’s credit score will be impacted by how long you’ve been in operation, your credit enquiries, Personal Property Security Register (PPSR) registrations and director information. You can improve your score by paying your bills on time, keeping balances low on credit cards and communicating with your creditors. Your personal applications for credit and accounts held in your name may also be checked to help the lender determine your risk profile. Being happy with your credit score and taking steps to improve it will put you in a strong position to begin your finance search.

2. Have a solid business plan

Lenders are most concerned about your ability to repay the loan over time. They’re not going to fork out and invest in your business if they doubt you’ll be profitable and successful in the future, so they’ll want to see proof-points that your business can stand the test of time.

A thorough business plan will make it easier for you to communicate your business vision, strategies and goals to lenders. Including information about how the money will be used and some cash flow projections will show you’re serious about your business and confident in your ability to repay the loan.

3. Know what type of loan you need

There are many different financing options available for businesses. To be eligible for most, you’ll need to have an Australian Business Number (ABN) and for some you’ll need to have been operating for a certain period of time (eg one year for most unsecured loans). You also might need to generate a minimum amount of annual turnover, which can range between $50,000 and $200,000 depending on the type of loan you’re going for. To decide which option to take, you’ll need to understand why you need the capital in the first place.

For example, if you need some additional funds to meet daily business expenses, you might want to take out a business credit card. Remember you’ll need to compare providers to score the lowest interest rate you can. If your expenses can fluctuate (maybe on days when you purchase stock) then consider a business overdraft account, which allows you to overdraw on your business account to a certain limit.

There’s no point approaching a lender for equipment finance if you’re just going to spend the money on inventory – it’s important to do your research so you apply for a product that will complement your needs.

4. Don’t leave it until the eleventh hour

All businesses need money to operate so if you’re short on cash, your business’s lifespan may also be short. If you know you’re going to need extra cash in the near future, start researching your loan options now! Approval for a loan can take anywhere between a few days and a few months, depending on the type of finance you’re applying for. It’s important to have some time up your sleeve so you’re not rushing the application and can wait out the approval process (without going bankrupt in the meantime).

When embarking on your search for finance, it’s important to practise due diligence to ensure you take out a loan that will suit your business needs. Understanding your credit history, having a solid business plan in place, researching your finance options and being prepared are simple ways to improve your chance of being approved so you can make your business vision a reality.