How to get a small business up and running as a parent with a disability

According to the Centre for Applied Disability Research, people in Australia with disabilities have a 13 percent rate of entrepreneurship, a higher figure than employed people without disabilities. This reflects findings in similar countries like the US and UK, where people with disabilities are turning to entrepreneurship as an alternative to traditional employment.

There are many reasons why starting a small business is a great idea for someone with a disability, especially a parent. You have the option of working from home, where you can be with your children. You don’t have to answer to anyone in terms of your schedule or how much time you need to take for your health. Perhaps most importantly, you have the flexibility to design a career and an environment that is perfectly suited to your life.

However, Australia’s low employment participation rate for people with disabilities show that there is still a ways to go. Many challenges face parents with disabilities on the road to entrepreneurship, but below are just a few simple ways in which you can get the ball rolling.

Look at Alternative Investment Schemes

Traditional loans and investment schemes present many barriers for people with disabilities, but alternative options are available. Things like peer-to-peer lending make funding easier and more accessible to everyone and can be a great way to get an initial investment for a small business.

Alternatively, there are various government grants available for entrepreneurs. Most of these are not specific to those with disabilities, but they are still a potentially useful resource if you are looking to set up a business. Finder has compiled a great guide to the best government grants and how to go about applying to them.

Get Transport

If you can drive, invest in a good vehicle if you are going to be a self-employed parent. If you are selling physical goods, you will want a car, van, or truck to transport them, and you may also need to drive people (or children) around in your day-to-day. Check for good deals on second-hand cars on Gumtree to find the perfect vehicle for your business needs.

Be Online

Nowadays, any small business worth its salt needs to have a solid online presence. This means a well-designed website, as well as social media channels. While you can pay someone to set these up and even manage them for you, it’s not too difficult to do on your own. Beautiful websites can easily be created with simple drag-and-drop interfaces, and social media channels can be linked for optimal sharing across the board.

When you create your website, make sure it is accessible. As someone with a disability, you will understand the frustrations of non-accessible web design, so set a good example by taking time to ensure your website can be used by everyone. Dreamhost has some great tips for doing this.

Create a Great Home Office

Over half of small businesses are run from someone’s home, and it is easy to see why. As well as saving on rent, working from home is especially convenient for parents with disabilities who require an environment tailored to their needs.

That said, it is not enough to simply put a desk in a corner of your living room. A home office should be a separate space within your house, ready for everything you may need to do great work. Check out these tips for a productive home office, from comfortable seating to lighting.

Do not be scared of entrepreneurship because you have a disability. Running a small business can be the perfect employment solution for someone who requires flexibility, independence, and a tailored environment, so it is worth taking that leap and persevering. Remember that you are not alone: there are plenty of resources and help available online, and your friends and family will be happy to support you in any way you need as you start your self-employment journey.

Thanks to Patrick Young and ableusa.info for this contribution.

Marketlend Academy: Why Marketlend is a “fierce advocate” for investors

In this video, Marketlend’s Founder and CEO, Leo Tyndall, explores why it is so important that Marketlend act as a “fierce advocate” on behalf of its investors, especially when it comes to protecting their investments. Watch the video or read the full transcript below.

We see a very significant need for a number of things. One is, obviously, we always want our investor support, but we also see that we need to be very diligent in enforcing debt and very diligent in making claims on insurers and ensuring that they understand the true risk so that the investor gets his funds back to the extent that’s possible. Obviously, if we find that if we were negligent or we were lazy about that point in our business, well then essentially you could say the wheels will stop.

You know, we we essentially look after our investors in that we see them as an integral part of our business, and we do see that they are leaving it – not leaving it to us – but they are a lot of he ongoing servicing role and the like is left to us. And they don’t want a situation where they put the money in and then they think that we’re sitting there, you know, having coffees in the background and not doing much and really not diligently ensuring that people pay on time, when I’m diligently actually collecting on debt or we’re not going to the insurer and advocating the case as to why they should pay.

And one of the things I think is very important there, it you look at the Royal Commission and you look at with banks now or you look at say, for example, the AMP scenario, you know shareholders is a bit of a similar example. Shareholders would like to think that AMP was doing the right thing for them. Not just protecting them, but also protecting the business. And then to discover that they weren’t and they were actually doing things that were contrary to the business. That’s something that we don’t want to ever be seen doing and we’re very cognisant of the need to do so.

And that’s why we do things like have a due diligence done by Deloitte every year. And that’s why we also have people like Clifford Chance review our legal documents. And that’s why we always invite investors, you know the larger investors do their own due diligence, and other investors while we have regular catch-ups or webinars or other items like that to really show them that we’re doing. And that’s why we have a newsletter to keep them updated as to what we’re doing.

Marketlend Academy: how to know if your hobby should be a business

5 Questions to Ask Yourself Before You Turn Your Hobby into a Business

- Is your great idea a hobby or a business?

When avid Australian gardener Matt Harris became frustrated with traditional plant watering methods, and the pests eating at his produce, he invented a self-watering, enclosed system called Vegepod. In 2016, Harris scored both publicity and an investment on the Australian version of Shark Tank. Since then sales have increased by more than 500 percent.

When Harris first come up with his idea, how could he have been sure it had the potential to become a business? Not every entrepreneur necessarily needs a huge investment to make a business work, but most beginning entrepreneurs will often find themselves wondering when their idea or hobby is ready to become a business. Whether you’re just at the idea stage, or have started selling already, answer these questions to help you decide whether you’re ready to hang a professional shingle.

- Can it make a profit?

If you want to make a career out of your hobby, first figure out if your idea can generate revenue. After all, a hobby is personal, but a business is commercial. There is also a difference between just making money, and making a profit. Write a business plan and crunch the numbers. Anticipate your revenue and expenses. Will you be in the black? Will you be enough in the black to make a living at this enterprise?

- Is there a customer base?

If you haven’t begun selling yet, don’t assume that just because you love your own idea that others will too. Conduct some market research to identify who would be willing to spend money on what you’re offering. Take advantage of social media and online survey tools to find your target audience. If you’ve identified a clear interested audience, then it may be time to test the waters by selling your product directly to that audience.

- Is there demand?

Identifying your audience goes hand in hand with demand. Signs of high demand include more sales than you are able to fulfill right away, overwhelming requests or positive comments online or on social media, or if you’re having to turn away customers because you’ve got more orders than you can fulfill. If you’re so busy trying to fulfill orders that it’s taking over your life, and you still feel like you’re falling behind, that’s a clear sign that people really want your business. This is the time to invest in your business and help it grow.

- Are you cut out for running a business?

Even if you’re sure that your business can make money, and you’ve identified both an audience and demand, your business will never take off if you don’t have the time to devote to it. Running a true business will require a full time commitment, and sometimes even more than that. Ask yourself first if this is something you’re willing or able to do. Not everyone is cut out for running a business. Signs that entrepreneurship is right up your ally include a desire to have a personal stake in what you’re working on, a dislike of rules, comfort with working hard, a tendency for seeking out problems and solutions, and a preference for independent thinking and a strong desire to be your own boss.

- Are you comfortable with risk?

Starting a business is by nature risky. Even if you truly believe in idea will make millions, there is always the possibility that your business will fail. But risk isn’t necessarily bad. The best businesses are often founded after multiple failures, so to get to a successful business probably means failing several times along the way. Be prepared for this. But make sure that this is a risk you’re willing to take, both from a financial and personal standpoint. Also be smart about taking the risk. Taking calculated risks means that you’ve planned every single detail, conducted all the research, and collected all the possible evidence that your business truly has potential. As long as you’ve done that then give it a go. Remember, you can’t learn to walk without falling.

Marketlend Academy: What is a loss reserve and how does it work?

Watch Marketlend’s Founder and CEO, Leo Tyndall, talk about Marketlend’s loss reserve, a important feature that protects investors. The text of his comments appears below if you prefer to read.

So a loss reserve for us in Marketlend is actually built on the basis of protecting against the possibility that we have someone who falls in default and therefore there is a differential or shortfall between say, in an insured position, the amount of insurance that’s paid and the amount that’s actually, essentially owed or in the case of an uninsured it’ll be that the assets themselves don’t sufficiently cover the shortfall to the amount that’s been advanced to the borrower himself, or the account holder. What we do with the loss reserve is, is that we essentially collect that loss reserve and if the actual borrower has paid on time at all times, they’ll get their loss reserve deducted off their balance when they owe the money.However, what we do do is, we actually hold that in a separate trust account and we enable that loss reserve to be assisting investors to actually protect against that additional risk they have that the insurance may have a shortfall. Not significant but, or that the actual underlying assets and the guarantor guarantee situation isn’t sufficient to cover that. As well as, possibly the fact that it takes a lot longer to actually collect the debt so therefore there is a need to cover that cost during that time.

Marketlend Academy: how to protect your business in a housing downturn

The state of the economy affects every business, especially small and medium sized enterprises. One issue that could be of particular concern for business owners is the recent decline in home prices.

Housing Market Conditions in Australia

Higher mortgage rates, increased lending regulations and financial scandals have led to a sharp decline in housing prices in the Australian market. Australian home prices have dropped for 11 months in a row, resulting in a 2% annual fall, the sharpest decline in property values in six years.

This is a business issue, as well as a homeowner issue, because reduced home values could have a serious effect on the financial interests of small and medium-sized businesses and, perhaps more importantly, their access to capital.

Impact of Reduced Property Values on Australian SMEs

A Duke University report states that “improvements in collateral values ease credit constraints for borrowers and can have multiplier effects on economic growth.” However, what happens when the opposite occurs and there are declines in collateral values? There are several ways that lower housing prices impact Australian businesses due to lower financial leverage.

Small and medium-size business owners in Australia may find it difficult to get financing from banks to start their companies, which is why it is fairly common for them to use residential real estate as collateral. The home’s value serves as protection for the lender in case the borrower is not able to repay the loan.

Previous property booms have facilitated lending, but the recent reduced property values will make it increasingly difficult to use homes as collateral to obtain small business loans. It will also be harder to utilize home equity lines or cash-out refinancing to finance startups or fund operations. Finally, the value of the guarantor’s personal assets will be lower, thus inhibiting their ability to use personal guarantees to secure business loans.

Strategies to Protect Business Assets Amidst Financial Instability

-

Separate Personal and Business Finances

The first step to protect your business amidst lower housing prices is to separate personal and business finances. Many Australian entrepreneurs have one bank account for dual purposes, which can put their personal assets at risk in the case of bankruptcy.

Linking your finances can also be detrimental to the business—if the lender observes that higher interest rates make it challenging to repay a mortgage, they may be less likely to offer new business loans. Alternatively, if a business is struggling, a lender may be unwilling to keep it afloat if there is insufficient property value to be used as collateral.

It is best to use different bank accounts and credit cards to separate business and personal finances. This will also make it easier to track businesses expenses and use them as tax deductions at tax time. While some expenses may overlap, such as car usage or a home office, designate a percent usage for business and pay it out of the specific account.

-

Utilise Secure Loans from Personal Funds

Many business owners use personal savings as capital injections to fund their businesses. However, should the company face financial constraints and go bankrupt, the investments will never be returned.

A better alternative is to make a secured loan to the business, using personal assets as collateral. Although this choice also carries some level of risk, if the business declares bankruptcy, the funds may be recovered through a liquidation. Additionally, there may be certain tax advantages for repaying a personal loan.

-

Maintain a Strict Budget

Businesses that are not properly budgeted for will likely require more cash infusions to sustain them through tough times. As it will likely be more difficult to obtain small business loans due to lower home values, it is important to maintain and stick to a budget for your business.

Keep detailed data about your spending and earnings and pay yourself a set salary—these steps will help you to understand your business expenses and anticipate and save for the future.

Financial concerns that affect SMEs are really everyone’s concern, since 90% of all Australian companies are small businesses that account for 33% of the country’s GDP and employ over 40% of its workforce. The current state of the housing market will no doubt affect entrepreneurship in Australia. However, with proper planning and implementation as well as guidance from a business attorney and a financial advisor, business owners should be able to sustain their companies and find funding for new business ventures.

Marketlend Academy: what we look for in investors

Watch Marketlend’s Chief Investment Officer, Jane Lehmann, talk about what Marketlend looks for in its investors. The text of her comments appears below if you prefer to read.

Marketlend has a very specific requirement in regards to its investors. Under the Corporations Act, we are required to only engage experienced, sophisticated, wholesale, official investors. So for an experienced investor, that really is someone who can demonstrate that they have, as the name suggests, experience in lending in these types of financial instruments, and truly understand the risks that they’re undertaking when they engage in the platform. Sophisticated is actually a means test related defining feature that you need assets of a 2.5 million. I think the inference there is they also are a more sophisticated and experienced investor.

The institutional investors have a different profile that they tend to be funds. Many of them are offshore. And for them they often have a specific risk profile that they’re interested in and we can customise that for them. We have a pool of loans that we have onboarded and we can work with them to understand what their risk tolerance is where there are risk sectors they’re not comfortable with, where they have an appetite and craft a portfolio for them.

The experienced and sophisticated investors have the opportunity to go on to the platform and make their own assessments. They can look at each loan that is presented and make their own assessment and take a view on whether that is something that appeals to them as an investment opportunity. And that is obviously why you need experienced investors, because they are making a financial decision.

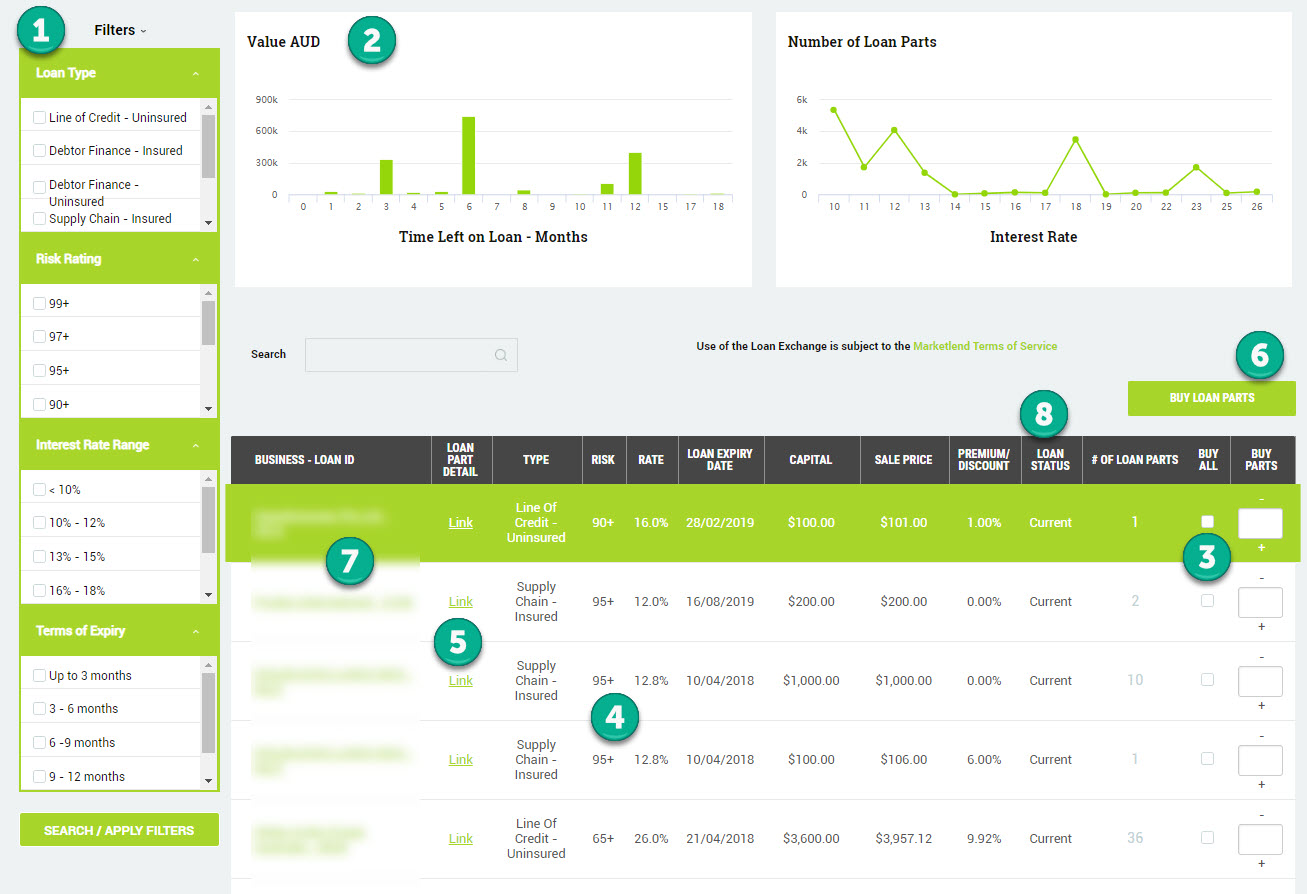

Welcome to the new and improved Marketlend Loan Exchange (Beta)

After ongoing investor testing and community engagement, we’ve created a new user experience built for your needs, the Marketlend Loan Exchange (Beta).

Making the most of Loan Exchange:

When you access the new Loan Exchange you will notice a number of key differences to the existing Exchange.

1.We’ve added some Filters to allow you to more easily select loan parts for sale that meet your criteria (depending on the device you are using and the size of your screen the filters will either appear at the side or in a drop down at top of exchange list).

2.We’ve added some graphs to show the make-up of available loan parts on the exchange. The graphs are responsive to changes in the Filters.

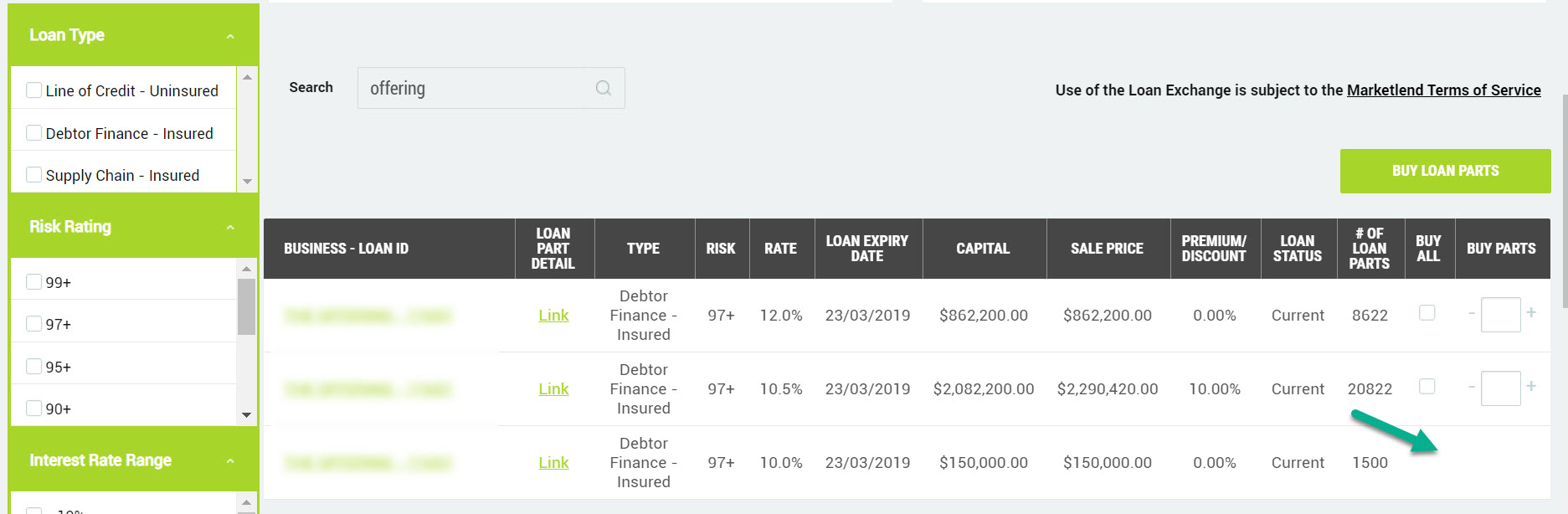

3.You can now choose to Buy All parts or a specific number of available parts without needing to view individual parts.

4.Loan Parts for sale are group by Loan/Interest Rate/Premium-Discount value.

5.You can still view all individual loan parts for sale by clicking on the Loan Part Detail Link.

6.Whichever option you choose – Loan Parts are bought by clicking the BUY LOAN PARTS button at the top or bottom of the list.

7.You can view Original loan details and updated Commentary by clicking on the Loan ID link.

8.We’ve added a column to indicate the Status of the loan – showing whether the loan is Current or is in Arrears.

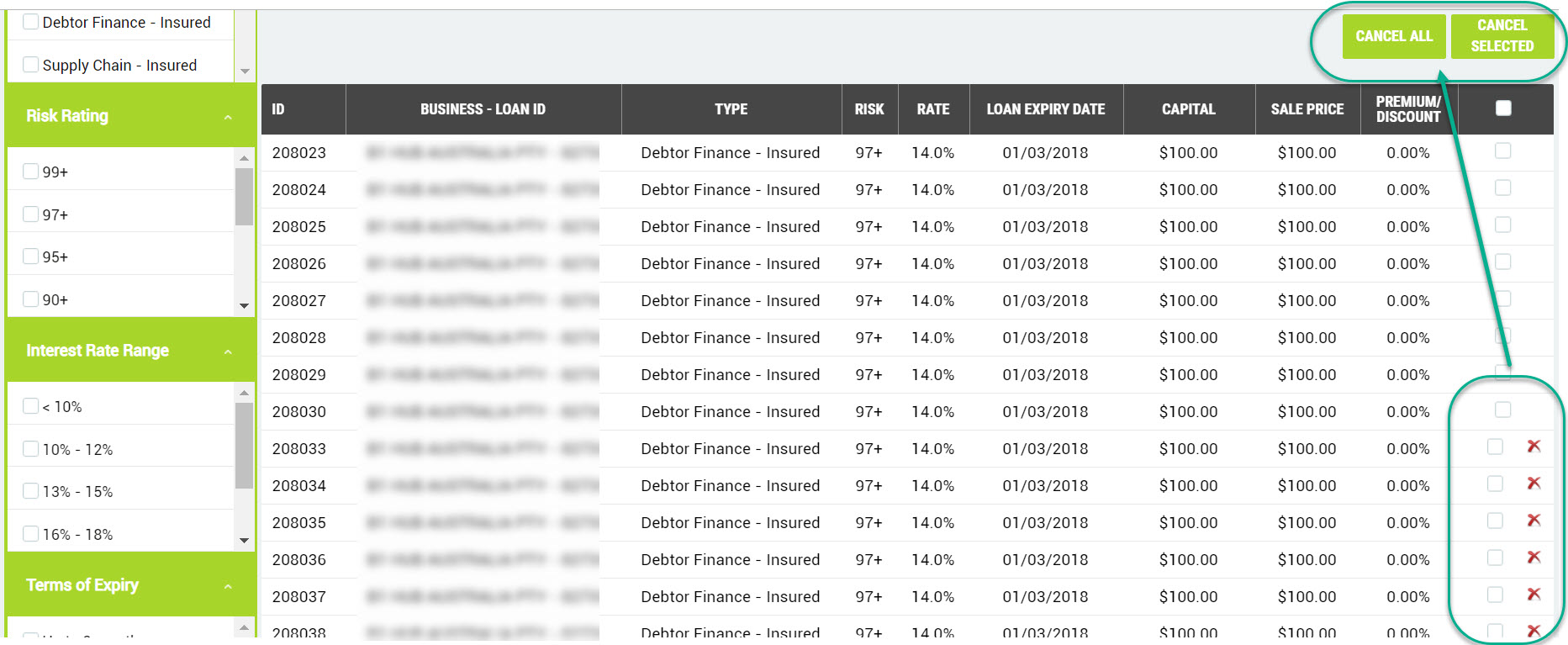

Cancelling Loan Part sales

If you need to cancel a Loan Part that has been put on the Loan Exchange for sale you can still do this from the Loan Exchange page.

If you own any of the Loan Parts for sale for a particular Loan you will see that the option to select Loan Parts to buy is not available.

To cancel any Loan Parts you just need to click on the Link to the loan part details. You can then choose which loan parts sales to cancel or select to Cancel All.

Marketlend Academy: Is Social Media Marketing Worth It?

Is social media marketing like using Facebook and Twitter still worth it? That’s a question many small businesses might be asking these days, considering these trends:

Globally, Twitter is reported to have lost 1 million monthly active users in the second quarter of 2018, while Facebook is expected to lose as many as 2.2 million users by 2022. In Australia as many as 1.8 million Facebook users have reportedly deleted their accounts. All this comes in the wake of the Facebook data privacy furor, which left users wary of social media.

How should this affect your use of social media in marketing your business? It’s more challenging, but still valuable, if you are mindful of these guidelines:

Have a strategic plan

Posting on any social network without a plan or understanding of what you want to achieve will get you nowhere. Decide on your goals and think about how social media can help you achieve them. Define your audience. Otherwise you’ll never break through all the noise, or reach the users that are likely to engage with your brand. Do your research, and keep in mind that the way you need to approach social media marketing may different for each social network.

Post engaging content

Yes, it’s harder to get noticed. But you won’t be noticed at all if you don’t take the time to plan great content that stands out. The same tricks of the trade still stand. You can always pay to advertise branded posts, but this doesn’t replace looking for ways to engage directly with users while promoting your brand, or posting something that helps you make an emotional connection with your intended audience. Offer information or advice that they can’t get anywhere else. You can also run contests, promotions and other fun games that attract engagement. Using social media management systems like Hootsuite can also help with planning.

Don’t over post

Don’t add to the clutter by tweeting randomly 24 hours a day. Your audience will just tune it out. It’s more important to make fewer, more strategic posts, and to engage in a conversation. Do your research by looking at what people are discussing, find something relevant to your brand, and try to target a few smart tweets or posts into the discussion. Make sure to take the time to respond to your audience.

Use visuals

Evidence shows that the content that performs best on Twitter and Facebook includes visuals. In 2017, Cisco estimated that video in particular will represent 82 percent of all website traffic in 2021. That’s why it’s crucial that you look for any opportunities to include photos, videos or gifs in your posts. These are the kinds of posts that are likely to get more views, and more clicks.

Branch out but choose wisely

Considering the negative trends impacting the two juggernaut networks, it may be a good idea to branch out. If you’re not already utilizing Instagram, consider developing a marketing strategy that includes it. Instagram is growing in popularity because of its reliance on the visual. In general, it’s a good idea to go where your intended audience goes. But make sure to limit your marketing to no more than 3 networks, because trying to do everything at once can make it harder for you plan and execute the right strategy for each.

The bottom line

Don’t swear off Twitter and Facebook just yet. But understand that you may have a tougher time being noticed, so it’s doubly important to make sure that you understand your target audience, posting engaging content that appeals to this audience properly and reflects your brand. Don’t make the mistake of just posting content into a vacuum and hoping it will get noticed. Amid all the noise, give those quality users that are still there a good reason to engage with you and your brand.

Marketlend Academy survey: how important is marketing to you?

Businesses have different schools of thought on how much time and money should be devoted to marketing and which approaches are most suitable for their companies. We’d love to hear about yours. Please take a few minutes to respond to this brief survey. We’ll share our findings and hope they create some interesting conversations that foster our growing sense of community at Marketlend.

Take the survey now.

Listen To The Investor Townhall

This past week, Marketlend ran an investor townhall. Transparency is integral to how Marketlend operates. Our investors expect it and we are committed to delivering on this promise. The investor townhall offered a chance to roll up our sleeves and explore issues that matter to the investor community.

We dug down into the mechanics of how we return principal in the event of a problem loan and the integrity of the Marketlend platform generally. There was ample room for Marketlend’s Founder and CEO to field questions and the result was a really engaging and hopefully enlightening look inside the how and why of this aspect of the Marketlend platform. Click above to have a listen.