Marketlend Academy: Marketlend performance for 2018

Each year it’s worth looking back to take stock, and we’ve been doing some of that at Marketlend – we’re happy to see that Marketlend performance in 2018 was as strong as it has ever been. Watch Marketlend CEO Leo Tyndall outline what it was that made 2018 a strong year for Marketlend’s investors and borrowers, and what’s making him excited about the future of peer to peer lending. You can also read the transcript below.

Video Transcription:

We had a great year. So from a volume point of view we’ve been very successfully growing our book. At the same time, from a risk point of view, we’ve been able to ensure that our book has grown, but not increased the negative effects of such a growth factor. So what we’ve seen is our default rates have actually reduced, it’s gone down from the 4.6% that we had for the year down to around 2-2.2%. But what we’ve also seen is we’ve been able to control the product that we produce and that means that investors have been able to get a great return. So the average return from a net point of view has been 10.2%. What we’ve seen is that we’ve been able to grow, and as I mentioned in other videos, that we’ve seen a growth of our book double compared to last year, so we’re up to $61 million funded.

We still look at December being a strong month as well, but what we’re seeing very much is also an increased focus of due diligence and implementation of some of the measures we brought in early in the year. We send out an external accountant if the exposure’s greater than $250,000, which has helped us significantly to really get to know our client, and then spending a lot of time interacting with our client post settlement. So we’ve put on settlement clerks, you could put it, so that they can interact with them post settlement so that we can increase the utilisation as well of the actual portfolio. So it’s been a great year for us.

As far as staff goes we’ve now got a total of about 35 people. In Australia we have around 15 to 16. I count that number because we only just put on two new people again today. So we’re continuously growing the actual support staff. We’ve also got the Philippines team which is a total of 14 people, and then we have developers all over the world. So it’s been a great year for us.

Marketlend Academy: How much should a small business spend on marketing?

Selling yourself is a part of every business, and marketing is the way it’s done at scale. But how much should a small business spend on marketing?

Like any question worth asking, the answer depends on your situation. Read on for some insight into what businesses are spending on marketing today, and what you need to think about before setting your own marketing spend.

Define your needs

What you want to achieve goes a long way to determining your budget. Your needs are different from other companies and will change over time. You may want to:

– Grow fast

– Grow sustainably

– Build brand awareness

– Maintain an established presence

These are all very different goals, with different associated costs. If you’re just starting out, every company needs a cohesive brand and a functional, professional website. Beyond that, your needs are completely custom.

With that caveat, there are some standards you can use to set your expectations.

How much should a small business spend on marketing?

Marketing budgets are normally measured as a percent of company revenues. To get a dollar amount from the percentages below, multiple them by a firm’s gross revenue.

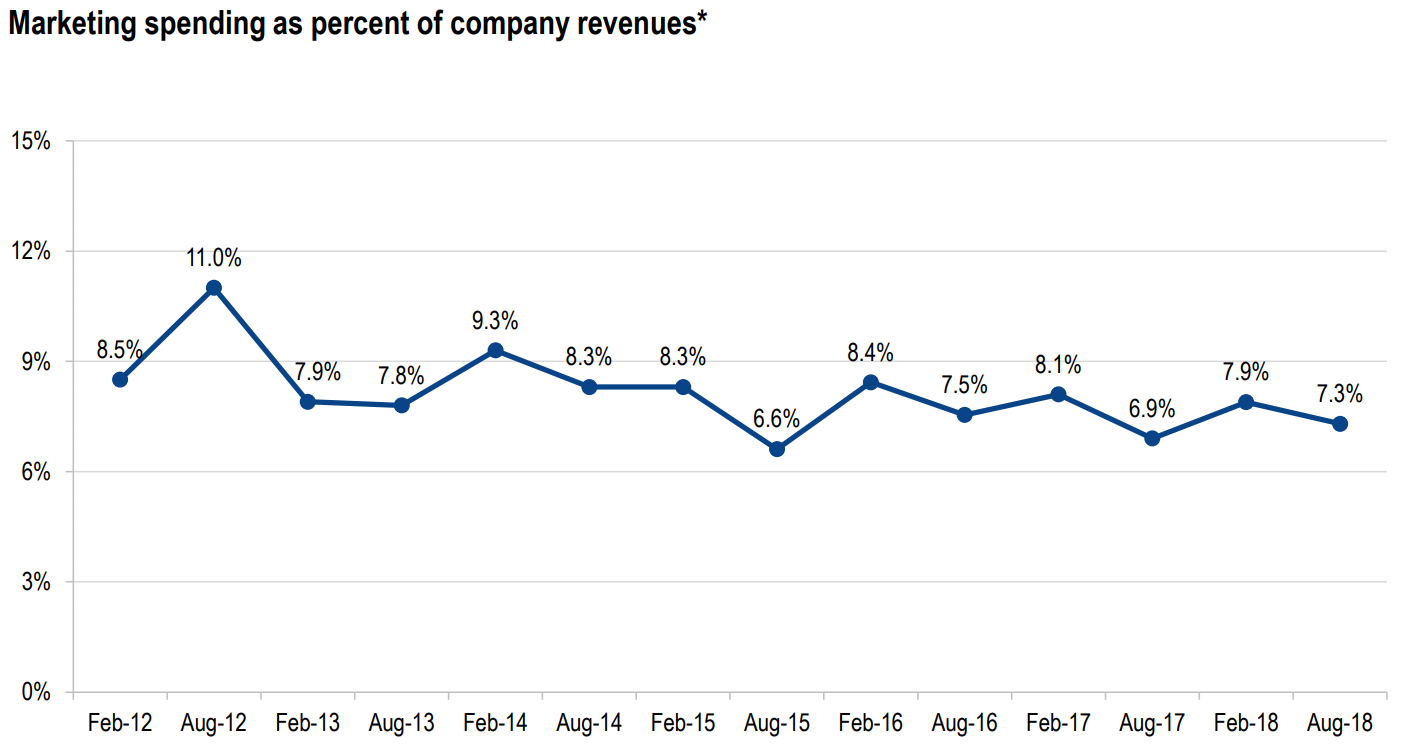

The August 2018 CMO Survey from the American Marketing Association found an average marketing spend of 7.3% of company revenues from 324 respondents across the US.

The chart below shows this is lower than recent years, but still within a typical range of 7-9% of revenue (source page 26).

Marketing for startups vs established firms

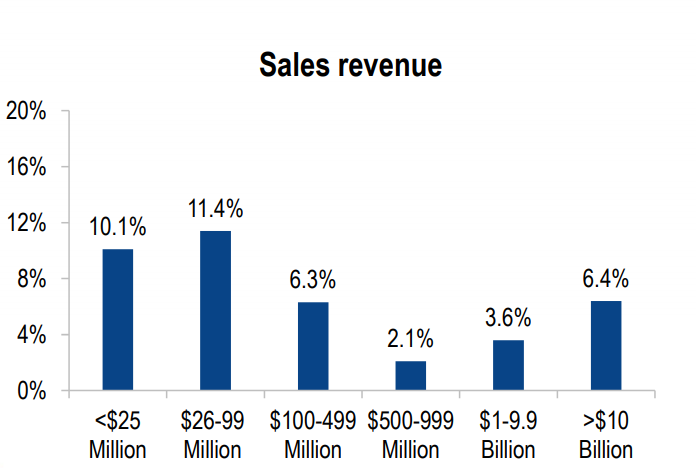

The report calculated average marketing spend by company size, as seen below (source page 27). Generally, smaller firms spend more on marketing than larger companies.

The first step of marketing is brand awareness, so smaller businesses without established brands are wise to spend more on marketing. Established brands can get away with a more efficient budget.

Ryan Flannagan of Nuance Media writes startups should expect to spend 12-20% of gross revenue on marketing, while noting a larger firm may only spend 6-12% of gross revenue on their marketing budget.

When the rules don’t apply

Knowing the rules helps you know when to ignore them, and a standard marketing budget won’t suit every company.

The CMO Survey breaks down marketing budgets as a percent of firm revenues by sector, below (source page 27).

Clearly there are situations where a big traditional marketing spend isn’t as useful. B2B services like mining, manufacturing, and professional services for instance typically rely on sales teams to attract new clients (with sales rarely included in marketing budgets).

Avoiding over-marketing

You can over-spend on marketing. First, there’s the opportunity cost of a high marketing budget that may be better spent on product or business development.

But there’s also the risk of growing too fast. If your marketing is too effective, you may face more growth than you can handle. That can cause serious cash flow problems that undermine other parts of your business, potentially sending you out of business.

Avoiding this isn’t difficult. First, don’t borrow more than what you need for the growth you can handle. If you’re using Marketlend to access flexible, peer-to-peer finance, don’t over leverage yourself. Make your repayments and you can always extend your line of credit later.

If you do have cash flow issues as you grow, a service like UnLock can provide extended payment terms to supercharge your cash flow, like a corporate version of buy-now-pay-later.

Pay it smart

The key element when setting a marketing budget is to be deliberate. Approach your marketing spend with a critical mind and a clear vision of what you want to achieve, and you’ll be miles ahead of the competition already.

Detecting cyber fraud as a small business owner

As a small business owner, you may have already had an experience with a scam targeting your business. It’s reported that Australian small businesses lost more than $2.3 million from cyber attacks in the first half of 2018, with nearly 18 per cent of small-to-medium-sized businesses in Australia having been impacted by a cyber scam.

While this seems like it would only affect you, it can also impact your customers. For example, hackers can “spoof” your business email account so their emails look like they belong to you. They can then contact your customers and request payments be made to a different account instead of your own. One Australian business recently reported losing $300,000 to such a scam.

In another version of this attack, scammers can intercept your correspondence with suppliers, and then pretend to be the supplier in order to get you to pay them instead. Other popular tactics include ransomware attacks in which your data is encrypted and held hostage until you pay the scammers a ransom. Thieves being thieves, you can never be sure if you’ll receive your data back even if you pay.

With so many ways you could be targeted, detecting cyber fraud is a top priority. To help you, here are several tips we suggest you follow to recognise and prevent a potential scam.

1. Never click on any links or attachments in an email unless you know the source and can verify its legitimacy. Poor spelling and grammar usually gives away fake emails.

2. Install anti-phishing software.

3. Never wire money to anyone you don’t know in person. Asking for wired money via services like Western Union is a very common scam.

4. Never fall victim to an urgent transaction. Typically, cyber attackers want to get your money as soon as possible so they can disappear. Confirm the transaction with your usual contact if things seem suspicious.

5. Make sure you keep back-ups of all your data. This will enable you to return to business as usual in the event you fall victim to ransomware without having to pay the attackers.

6. Check the URL of any website you’re asked to access, especially ones where you have to enter sensitive information, to make sure the website is legitimate. A fake URL may look similar but can have spelling errors. If it is hyperlinked, you can check the website by hovering your mouse over the link. Otherwise, type the address in the search bar yourself if it’s a website you know, such as an online banking portal.

7. Make sure that any financial transaction you engage in online requires you to enter your details only after the URL changes from “http” to “https”, this means the connection is secure – all Australian bank log-in pages are https.

8. Limit who in your business has access to sensitive financial details to those who absolutely require it.

9. Trust your gut. If something feels odd, or you see an offer that seems too good to be true, then it probably is.

10. Report suspicious activity. Most Australian banks, telcos, and energy providers – the industries most frequently impersonated by scammers – have sections on their websites where you can report a scam. They also publish details of current illegitimate activity.

Marketlend Academy: 2019 Outlook – The big challenges for 2019

2019 looks like another good year for Marketlend, which is great news for you. A strong year for Marketlend means even more flexible finance for SMEs to grow, and more great opportunities for investors.

Watch Marketlend CEO Leo Tyndall’s 2019 outlook, what he’s excited about, and what he sees as the biggest challenges in the year ahead. Or, read the transcript below.

Video Transcript:

We’re looking at quite a very positive year ahead. We’ve recently engaged two new sales team who are ex American Express and we’ve seen a significant pickup in our origination volumes in the last year. So we see that in the last month, in November, we did 5.2 million and we see that we’re possibly looking at similar numbers or even doubling those numbers going forward.

With the avalanche of these new products we’ve brought out, essentially UnLock as well as GreenLend, we see a bit of energy there coming back from an investor base as well as from the borrower base. And so what we see is from that side, a very exciting year. From the risk side we have added additional measures to protect our position, or the investor’s position, and so where we see with that is that we see a continued good performance from the book and also seeing that our clients are actually gonna grow with it.

As far as the economy goes, there are some stresses that we are cognisant of and concerned about, especially the construction industry as well as the possible retail industry as the continual issue with the fact of the online businesses growing so well and the retail business, sort of, lease holds being a bit of a struggle. And so what we are focusing is on making sure that we try to diversify away from that as much as possible, or at least when we see those opportunities we ensure that we actually have additional protections for the underlying investors.

Marketlend Academy: Small Business New Year Resolutions

A new year, a fresh start!

As you think about New Year resolutions in your personal life, consider also what new goals you can also apply to your business in 2019. New Year resolutions can include reevaluating goals to make sure that you are growing and staying on track. They can also include getting important logistical tasks out of the way for the year so that you can focus on what’s most important for the rest of the year.

What are your small business New Year resolutions in 2019? Here are a few suggestions:

- Take a fresh look at your business plan

You think you know where you want your business to go, and you’re already on the way there. But now that you’re back in the office from the holidays, it never hurts to take another look at your business plan with a fresh set of eyes. It’s okay to change goals slightly from year to year depending on the progress you’ve made last year, or based on changes in the market. Make sure your business plan is always in tune with your customers and with the market.

- Decide on new goals and how to accomplish them

Once you’re sure your business plan is exactly what you want, then evaluate your progress in 2018 and develop your goals for 2019. Think about what kind of business you want to have by January 2020, and ask yourself what you need to do to get there. This may involve things like hiring new staff, upgrading your office space, or investing in more advertising or marketing. Figure out the specifics of what needs to be done, and how you will go about it.

- Work out a 2019 budget

This one goes hand in hand with number two. Once you know what you need to do, calculate how much money you’ll need in order to achieve it, and plan for where those funds will come from. Don’t get your hands dirty before you have a budget, or you risk overspending and ending up with a deficit. Make sure you have the money to tackle all your goals, whether it will come from personal funds, the profit from your business, loans, or from outside investors. If you need more funds, then plan for how you’ll acquire them. Marketlend is on hand to help you acquire financing by connecting you with the right investors.

- Update the online side of your business

These days you can’t run a business without having the right presence online. Brick and mortar sales are still important, but making sure customers recognise you and can find you online is a must. As 2019 begins, it’s a good time to check your Google analytics to make sure you’re attracting enough web traffic, and that this traffic is translating into sales. Look at how your online customers behave in order to see if you need to change the way you target them. Also check if your website is properly optimised for search engines, and that you’re well-positioned on the major social media sites. If you already have an online brand growth plan, then revisit it and make sure you’re on track to where you want to go.

- Evaluate how you use resources and energy

Have you ever thought about how you use your office space, or how much energy your business consumes? At the start of the year, it’s a good idea to check that no space or supplies are being wasted, and review how much power you’re using. This can include things like moving to a more space-efficient office, reducing supplies that you’re not using, changing your electricity provider, or even looking into using alternative energy sources. Reevaluating what you consume and how you consume it can translate into major savings, which equals money you can put right back into your business.

Once the year starts in earnest, day-to-day business needs often take precedence and its hard to carve out time for any planning or business self-reflection. With the start-of-year seasonal lull many businesses experience, its perfect time to take a step back and map out the year ahead.

Marketlend Academy: Government, SMEs, and a business comparison rate

Government getting too heavily involved in business isn’t always a good idea, as it risks eroding the free market’s power to innovate. However, there is a place for regulation that gives all business the best chance to succeed.

When it comes to small business lending, Marketplace CEO Leo Tyndall says one simple change would make a huge difference to Australian SMEs, the requirement of a small business comparison rate. Watch the video or read the transcript below to learn how government can unlock the potential of small business.

Video Transcript:

I’m never a big fan of pushing government to do a lot of things because the the more involvement government has on business the danger it is that it actually doesn’t operate in a capitalistic environment. But what I do say the government need to do is ensure that there is a level playing field. To ensure that the SME’s able to make the right decisions.

What I mean by that is the SME itself should be able to within a very short period of time look at all the finance options and then go, “Yes. This is the price. This is the real price of my funds.” And to do that at this present moment, there isn’t a framework for every SME to be able to give a comparative rate.

So if we look in the mortgage market, you go and look at the advertising in mortgage market, you can say, “Well what’s the comparison rate?” and you can match them all and put ’em in a line and then say, “This guy’s got the cheapest rate ’cause this is his comparison rate and it’s the lowest.” We don’t have that in the SME market. And that’s what’s needed.

The SME market needs the requirement. What the government needs to do is say to SME lenders, “You must give a comparison rate. You must tell them what is the real cost of funds.” [The] very immediate time that [SMEs] touch base with you you should say, “This is what your cost of funds will be”, and so therefore the SME can quickly make a decision whether it is the cheapest or more expensive. Now you can say that you’re more expensive than the others and say these are the reasons why you’ve got all these other benefits. But you do need to give a true, clear price.

And that’s unfortunately not available at this time. So this is where I think the government really does need to step in and it’s only an extension of the Trade Practices Act or the the consumer laws. So it’s not like there’s a lot that they need to do there.

Marketlend Academy: The Problem With Australia’s R&D Tax Incentive

Small and medium sized business don’t get a lot of tax incentives in Australia, both compared to larger firms and overseas competitors. One of the few SMEs can claim is the Australian Reasearch & Development tax incentive. But Marketlend CEO Leo Tyndall says the R&D tax incentive needs to be improved for SMEs. Watch the video or read the transcript below to find out how.

Video Transcript:

One of the issues than an SME has when they start up for the first one to, say, five years is that the only tax breaks that are available to get is if they’re determined to be an R&D company or something similar. Now ironically, if you’re an R&D company in Australia, unless you can prove that your R&D is out of Australia, and for a lot of these, especially in even our space where the technology’s not here, it’s offshore, you can’t get the benefit. You can’t get a tax break. So if you look at other countries where, you know, SMEs or people have actually started up some type of new business that is a new concept, they’ve been able to get that break and that enables them to grow.

I mean, the Googles of the world and all of these type of guys. You know, this is something that the government should really have a better look at and say, “Okay. We’ve got these incentives, these grants, and R&Ds, but if the R&D grant is only working for if the R&D’s done here, how can I do that when the R&D doesn’t come from here?” What you want to say is, “Okay. Are they taking R&D from offshore and then putting it in here so that then they can develop their own R&D here?”

Marketlend Academy: How to Hire for Your Small Business

Your small business is thriving. You’re growing. You need to hire, but unsure where to begin and what resources are available. The right hire can boost your business productivity and profitability. The wrong hire can be an expensive and time-consuming mistake. Here are a few best practices for hiring employees for your small business.

1. Define the position

Before you set out to hire, ask yourself:

- What challenge is my company grappling with that a new hire could solve?

- Is this a long-term job or a temporary, contract position?

- Am I open to a remote hire?

- Can I afford a new person without damaging my bottom line?

Research each question and talk with your team. A remote hire is cheaper, but your team might struggle with the distance. A contract worker can also be a cheaper option, but if your company is growing, you may just need a full-time on-site staff member. Evaluate the full cost, including salary, benefits, taxes, workspace and equipment before you make your decision. Requirements can vary widely across regions and countries. Australia, for example, has a range of requirements that can get complicated very quickly, the Government’s Fair Work Ombudsman has a page devoted to this that includes a Pay Calculator.

2. Set your hiring budget

Hiring can be an expensive endeavor. Before you advertise the position, make a spreadsheet with the following categories:

- Job boards and advertising – Note the cost of each post per site. If you have a premium membership that lets you post for free, write the zero.

- Assessment – Skill tests run by an external company will have a flat rate per candidate. Multiply the number of applicants you want tested by the exam price.

- External recruiting – Consider outside organizations who can search and hire for you and record the cost. Remember recruiters typically take a percentage of the employee’s compensation, but this amount will usually be refunded through a “claw back” fee if the hire doesn’t work out in an agreed period of time.

- Human Resource hours – Multiply the hourly rate of each person on your hiring team by hours spent on resume reviews, interviews and follow-up.

Keep in mind that the cost to recruit is unpredictable. Record your actual costs after the process is complete and keep an eye on your hiring budget from month to month.

3. Write the Job Post

A good job post should be a clear description of the job. It should entice candidates with the essence of what the company has to offer with these basic elements:

- A clear title for the position

- A thorough overview

- The desired qualifications or experience level

- Information about how to apply

- For local hires, try Seek

- Quality remote hires can be found at WeWorkRemotely, RemoteOK, and FlexJobs

Check your job ad on any board or website to make sure your description is displayed properly and any associated links work when clicked.

4. Make the Most of Social Media

The typical company today has a minimum of seven social media accounts. Make the most of these spaces and attract your next employee with the contacts you already have at hand.

- Focus on what sets you apart – draw candidates in with industry news, updates on projects and photos of your team. Give them a peek into your company before the official application.

- Highlight value – think about what your employees love about their work. For example, UPS tells potential hires they can “Deliver wishes” as an employee. Play up the best qualities of your company and share them on all your social channels.

- Find niche networks – look for the online forum specific to your position. If you need an SEO expert, you want to post on Freedom with Writing. Developers prefer StackOverflow while Moz is home to marketers.

5. Review resumes

Resume and cover letter reviews can be a good chance to get to know each candidate. Each is a chance to see how much care a candidate put into her application and what she can add to your company.

- Look at the big picture – Read through cover letters with care. Is this a form letter or a piece written directly to your company? Review the language choice and professionalism used in the text to make sure this person knows your industry. No cover letter? Move on.

- Think in terms of Yes/No questions – Does the candidate have the qualifications you specify in the job description? Can the candidate be trained?

- Red flags – Long, over-written descriptions that take up a lot of space, spelling or grammatical errors or general descriptive language that doesn’t really tell you anything, like “a leader” or “enthusiastic” are all red flags that should give you pause.

- Find your favorite – Take the applications you like best and start the next phase of the process.

6. Interview candidates

Good job candidates see the interview process as an opportunity to talk about the job, the company, and why they would be a good fit. An interview should be a comfortable, professional conversation. But be prepared with specific questions that will help you know whether the candidate meets your needs. Additional tips:

- Assess and test – Check for a skill match with technical questions or a skills assessment test as a part of the interview. This way you know how each person works and how fast they can produce.

- Keep a goal in mind – If you want to know how a worker interacts with authority, try “What kind of oversight would an ideal boss provide?” Autonomous workers will want an absent boss while collaborators prefer an accessible leader.

- Ask for questions – At the end of the interview, give your visitor a chance to ask you something. You want an employee who asks about future projects or milestones, has questions about you as a boss or office culture.

- Watch for body language – Look for moments when your candidate’s face lights up with enthusiasm or sits forward. These are signs of deep passion.

- Define your culture – Think about what kind of office you run. Do you value teamwork? Place a premium on collegiality? Or are you looking for a lone wolf who can just get the job done? Make sure your candidate fits your company culture.

- Hire people you like – Do you like the candidate? The interview should be an opportunity for you to see whether there is any professional rapport. You’re building a team, after all, that needs to want to work together. And you’re the head of it.

7. After the interview

Narrow down your choices to two to three candidates. Start with your top candidate and do your research.

- Fact check – Is the work history accurate? Has your candidate exaggerated her experience or invented a past company?

- References – Call them. Ask them to describe their professional relationship and be specific about why the candidate would be a good fit for the job. Strengths and weaknesses. Ability to work with people. Attention to detail and deadlines. Ask them what else you should know about the candidate.

- Other calls – Do you have mutual colleagues who might have insights on this person? These calls can be more helpful than the listed references.

- Keep in touch – Potential recruits with good skill sets will get snatched away fast. Maintain a correspondence with your top two or three and let them know they are still in the running.

8. Extend the Offer and Negotiate

You have your favorite, you’re ready to hire, now what?

- Act Quickly – Decide as fast as you can so you don’t lose your hire to a competitor. Aim for one to three days after the interview.

- Put the job offer in writing – the whole job and all the details. Include any policies your company upholds including sexual harassment, dress, extra work days or hours.

- Make the Offer – Schedule time to present the offer. In person is always best, but not always possible. Then, present it with enthusiasm! Make sure the candidate understands all the elements of the offer, both in writing and in your presentation.

- Set a Deadline for a Response – Give the candidate time to consider the offer, discuss it with family, etc. But set a deadline for a response.

- Negotiate – If the candidate wants to negotiate salary or other elements of the offer, be prepared. This is where your budget comes in handy. Be flexible, but know what your budget will allow you to offer.

- Make the Hire – If the candidate accepts the position, you have a new hire! If not, move on to your next resume and keep going.

You did it – you’ve made a great hire! And you now have a bank of resumes that might come in handy for future hires. Be sure to save them and note the ones that stand out.

Thank each of the candidates you interviewed with a personal call, if possible. Send email responses to all the candidates who applied for the position, thanking them for taking the time to apply and letting them know the position is filled.

The hiring process is a difficult one, for all involved. How you handle the candidates you don’t hire is as important as how you handle the ones you do. Your professional courtesy in this process will serve you well in the long run. You’ll likely be making more hires down the road, and word will travel about what it’s like to apply for a job with your company. Make sure it’s a good experience.

Marketlend Academy: How Do We Assess Potential Borrowers?

Marketlend CEO and Founder Leo Tyndall wants his investors to know that no one applies for a loan on the site without a thorough review of their financials, and that transparency and responsibility –and ultimately care for the underlying businesses that borrow– drive Marketlend’s mission. In this video, Tyndall breaks down what his team looks for in a potential borrower’s financial profile. The key for Marketlend is the long term health of the businesses it lends to, because healthy SMEs thrive as businesses and as borrowers –that’s why assessing what is reasonable, fair and sustainable in terms of repayment ability is so critical. Click the video to hear about the process. Prefer to read? Scroll down for the transcript.

So, Marketlend requires at least one year’s financials. We look at their debt servicing ratios, we actually look at what it looks like before the loan and after the loan. We typically have a hurdle of 1.5% on debt servicing after the loan. We also turn around and we point out to the borrower that we’re doing a monthly charge, on the uninsured we may do weekly, but what we do, do is, we look at their ability to repay.

We don’t want a situation where we’ve advanced the money, and then they can’t pay us back. So what we’ll do is have a look at all their cash flows, we also look at, essentially, a new structure in the way of we look at their full cash flows, their expenses and then say, “Okay, what is their true flowing cash that they can afford to pay it?”

And we will go through their bank statements as well, so we will go through their bank statements, and for example, on a supply chain, we may turn around and someone says, “I want 100,000.” We look at their bank statements and say, “You couldn’t even pay 100,000 back to us on three months on the supply chain, so why would we advance you that money?”