Category Archives: Borrowers

Leaving the Banks Behind: How Planet Ark Power made solar profitable with Marketlend

Upfront costs and unconventional financials have held back the expansion of businesses transforming our energy markets and introducing new ways of delivering electricity.

That’s what happened to Planet Ark Power, an engineering organisation which combines modern PV solar panels and batteries with AI powered software to ramp production up or down based on demand from the electricity grid. With a system that is cash flow positive from day one, Planet Ark Power installations help businesses turn energy from a liability into a revenue stream, as well as providing energy security.

But not too long ago, Planet Ark Power struggled to get the funding they needed to grow.

“5 Months of Hell” – The role of the right finance

Rapid growth brings rapid change, and Planet Ark Power needed a line of credit to cover the cost of those changes. But Executive Director Richard Romanowski says his experience with getting finance from the banks was less than ideal.

“The bank put us through five months of hell, then said ‘go make your sales targets for the year and come back to us’. The banks will only give you money AFTER you’re successful, with no regard for how much energy it takes.

“That’s when Marketlend came to the rescue. They asked us to explain what we were doing and our business prospects. When they understood our challenge, they said ‘this is a great opportunity’.”

By looking solely at past numbers, investors can easily miss high value opportunities like Planet Ark Power. The Marketlend platform makes up for what’s lacking in the traditional lending model by providing investors both a quantitative and qualitative assessment of each company.

In doing so, small to medium enterprises have more flexible access to fast finance, allowing them to take advantage of growth opportunities in their sector.

How Marketlend made growth simple

Through the Marketlend platform, Planet Ark Power borrowed $500,000 from 50 lenders, which Romanowski says has been a game changer for the business.

“The cost of client acquisition is huge. We’ve gone from $30,000 sales to $10 million sales, and each one is a massive learning curve – building new systems, new sales approaches and so on.

“I have a 5-star contract but I have to wait 60 days to get paid. With a customer base growing and changing so fast, I need cash flow to handle it.”

No more missed opportunities

Marketlend puts sophisticated investors in touch with high potential opportunities that fall through the cracks of traditional lenders. It avoids the many pitfalls of a peer-to-peer lender, because it is a vetted, thoroughly transparent lending platform.

“Marketlend actually cares about your business. They really want to know what you are doing,” Romanowski says.

“They take a bit of a punt with you – not in a lender-of-last-resort way, but in a way that actually understands the risk and reward.

“We now have a $500,000 line of credit and are looking to increase it. When we first went to Marketlend we had 25 staff, today we have 35. Not only that, the size of the projects are growing fast.

“Because they really understand your business, they can unlock the opportunity.”

Marketlend Academy: How much should a small business spend on marketing?

Selling yourself is a part of every business, and marketing is the way it’s done at scale. But how much should a small business spend on marketing?

Like any question worth asking, the answer depends on your situation. Read on for some insight into what businesses are spending on marketing today, and what you need to think about before setting your own marketing spend.

Define your needs

What you want to achieve goes a long way to determining your budget. Your needs are different from other companies and will change over time. You may want to:

– Grow fast

– Grow sustainably

– Build brand awareness

– Maintain an established presence

These are all very different goals, with different associated costs. If you’re just starting out, every company needs a cohesive brand and a functional, professional website. Beyond that, your needs are completely custom.

With that caveat, there are some standards you can use to set your expectations.

How much should a small business spend on marketing?

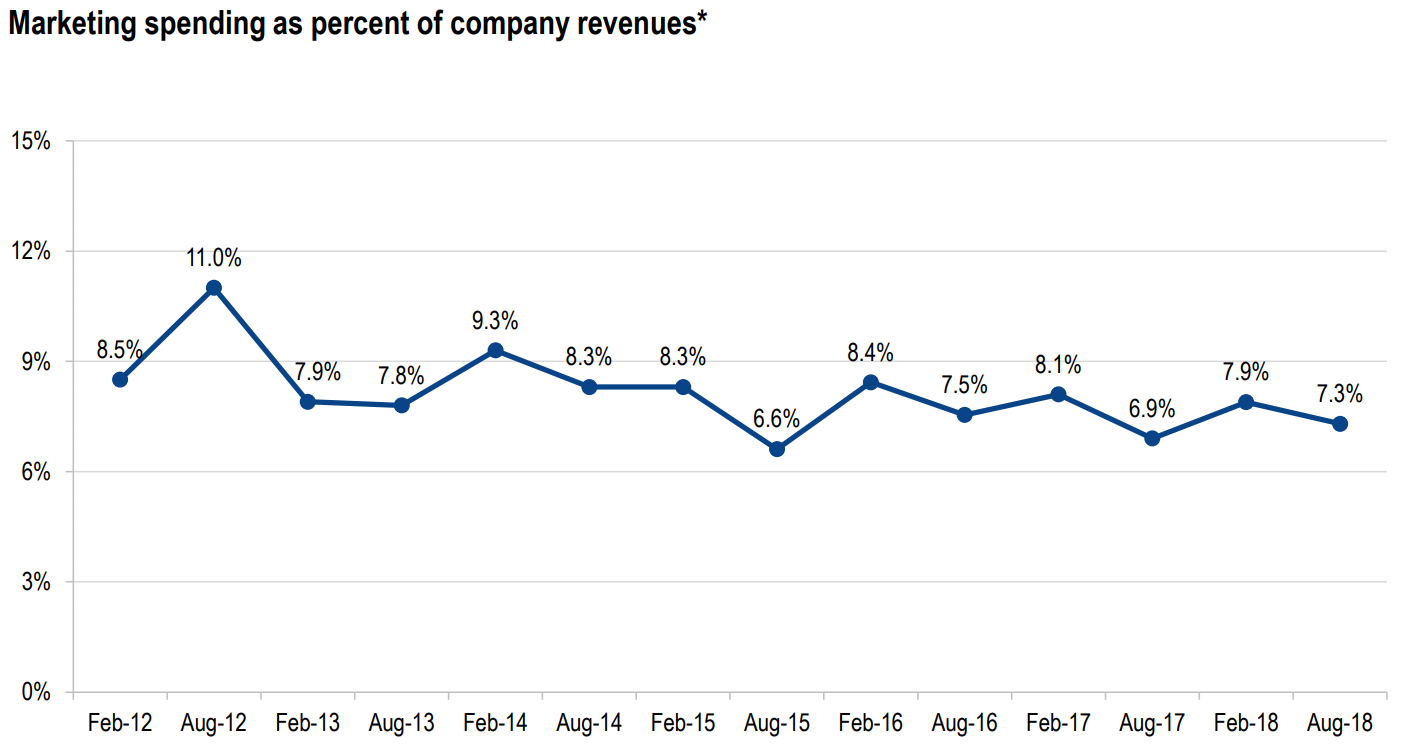

Marketing budgets are normally measured as a percent of company revenues. To get a dollar amount from the percentages below, multiple them by a firm’s gross revenue.

The August 2018 CMO Survey from the American Marketing Association found an average marketing spend of 7.3% of company revenues from 324 respondents across the US.

The chart below shows this is lower than recent years, but still within a typical range of 7-9% of revenue (source page 26).

Marketing for startups vs established firms

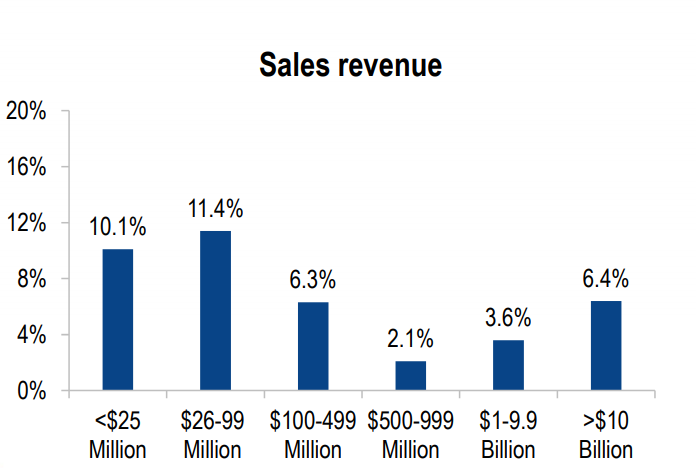

The report calculated average marketing spend by company size, as seen below (source page 27). Generally, smaller firms spend more on marketing than larger companies.

The first step of marketing is brand awareness, so smaller businesses without established brands are wise to spend more on marketing. Established brands can get away with a more efficient budget.

Ryan Flannagan of Nuance Media writes startups should expect to spend 12-20% of gross revenue on marketing, while noting a larger firm may only spend 6-12% of gross revenue on their marketing budget.

When the rules don’t apply

Knowing the rules helps you know when to ignore them, and a standard marketing budget won’t suit every company.

The CMO Survey breaks down marketing budgets as a percent of firm revenues by sector, below (source page 27).

Clearly there are situations where a big traditional marketing spend isn’t as useful. B2B services like mining, manufacturing, and professional services for instance typically rely on sales teams to attract new clients (with sales rarely included in marketing budgets).

Avoiding over-marketing

You can over-spend on marketing. First, there’s the opportunity cost of a high marketing budget that may be better spent on product or business development.

But there’s also the risk of growing too fast. If your marketing is too effective, you may face more growth than you can handle. That can cause serious cash flow problems that undermine other parts of your business, potentially sending you out of business.

Avoiding this isn’t difficult. First, don’t borrow more than what you need for the growth you can handle. If you’re using Marketlend to access flexible, peer-to-peer finance, don’t over leverage yourself. Make your repayments and you can always extend your line of credit later.

If you do have cash flow issues as you grow, a service like UnLock can provide extended payment terms to supercharge your cash flow, like a corporate version of buy-now-pay-later.

Pay it smart

The key element when setting a marketing budget is to be deliberate. Approach your marketing spend with a critical mind and a clear vision of what you want to achieve, and you’ll be miles ahead of the competition already.

Marketlend Academy: Tips to pay off business debt

While some debt is necessary to fund a business, if you’ve ever found yourself turning to a personal credit card to stay afloat… it’s time to stop for a moment and consider your options.

Here’s a sobering statistic: Last year, a survey of 1,200 Australian SMEs showed about two thirds of small business owners rely on credit card debt to maintain cash flow in their business. Just two years earlier, the Australian Bureau of Statistics found only a third of SMEs would use credit cards to maintain cash flow.

That means the number of businesses turning to credit cards to keep their businesses afloat has doubled in two years.

While there’s a certain convenience to using the credit card, the ensuing interest rates can put a business under even more financial pressure. Instead, here are a few tips to smooth out cash flow, and start to pay off business debt in your firm.

- Are your costs too high?

Reevaluate your regular expenses. Are you paying too much for supplies or materials? Research new suppliers and see if you can get similar materials elsewhere for less.

You could also reduce your office space and sell off equipment you don’t need or no longer use, or look into reducing your energy consumption.

This will result in savings you can put toward reducing your debt, or for maintaining cash flow in lieu of entering into even more debt.

- Can you buy now, pay later?

When looking at supplies and materials, have you considered services like Marketlend UnLock? Launched late last year, UnLock is similar to consumer ‘buy now, pay later’ models like Afterpay, except it is designed for small businesses.

In effect, Marketlend pays the supplier upfront for the materials, then gives your SME extended credit terms to pay the amount back – typically 90 days instead of the usual 30-day time frame.

This longer credit term allows businesses more time to repay, thereby smoothing out cash flow.

- Can you prioritise paying off your debt?

If you’re going to owe money, then you should know how much you owe and to whom. If you’re accumulating so much debt that it’s becoming challenging to keep track of what payments you must make every month, it’s time to take stock of your debt in order to prioritise your payments. Generally, when looking at loans it’s best to pay off those with the highest interest rate first.

Also consider consolidating loans if possible. Not only are consolidated loans easier to manage, as there are less people to pay, but you can typically find a lower interest rate – depending on the circumstances.

Start Today

This is by no means an exhaustive list, butit’s the three best places to start. If the debt your business carries is slowing you down, the best thing to do is take steps to pay it down today. Even if those steps are small at first, they’ll compound into giant leaps over time.

Marketlend Academy: Government, SMEs, and a business comparison rate

Government getting too heavily involved in business isn’t always a good idea, as it risks eroding the free market’s power to innovate. However, there is a place for regulation that gives all business the best chance to succeed.

When it comes to small business lending, Marketplace CEO Leo Tyndall says one simple change would make a huge difference to Australian SMEs, the requirement of a small business comparison rate. Watch the video or read the transcript below to learn how government can unlock the potential of small business.

Video Transcript:

I’m never a big fan of pushing government to do a lot of things because the the more involvement government has on business the danger it is that it actually doesn’t operate in a capitalistic environment. But what I do say the government need to do is ensure that there is a level playing field. To ensure that the SME’s able to make the right decisions.

What I mean by that is the SME itself should be able to within a very short period of time look at all the finance options and then go, “Yes. This is the price. This is the real price of my funds.” And to do that at this present moment, there isn’t a framework for every SME to be able to give a comparative rate.

So if we look in the mortgage market, you go and look at the advertising in mortgage market, you can say, “Well what’s the comparison rate?” and you can match them all and put ’em in a line and then say, “This guy’s got the cheapest rate ’cause this is his comparison rate and it’s the lowest.” We don’t have that in the SME market. And that’s what’s needed.

The SME market needs the requirement. What the government needs to do is say to SME lenders, “You must give a comparison rate. You must tell them what is the real cost of funds.” [The] very immediate time that [SMEs] touch base with you you should say, “This is what your cost of funds will be”, and so therefore the SME can quickly make a decision whether it is the cheapest or more expensive. Now you can say that you’re more expensive than the others and say these are the reasons why you’ve got all these other benefits. But you do need to give a true, clear price.

And that’s unfortunately not available at this time. So this is where I think the government really does need to step in and it’s only an extension of the Trade Practices Act or the the consumer laws. So it’s not like there’s a lot that they need to do there.

Marketlend Academy: SMEs are the true north for the 2019 election

Each new year brings a chance to make changes for the better, but with a federal election just months away, this year is one of the more unpredictable. One thing is certain: SMEs will play a key role in the development of the major parties’ business policy, and for the resulting direction of the economy.

With an early budget, the election will probably be held in May, and at this stage it’s not likely to be a tight race. A December Newspoll found 55 per cent believe Labor will win, while just 24 per cent back the government for re-election. But even strong polling guarantees nothing, so both parties will be desperate for support, and every coherent group of voters will be up for grabs. SMEs are high on the list, representing everything from Mum and Dad operations to industry leading firms.

That’s a mixed blessing. While both parties courting the sector should lead to progressive policies that benefit both business and the economy, the promise of wholesale change can increase uncertainty. A closer than expected election could also result in political uncertainty, which would cause additional anxiety for the economy as a whole. That could have a pronounced impact on SMEs, especially if the availability of capital is affected.

For SMEs to enjoy smooth sailing after the election, both major parties need to be clear on what their policies are, and why they believe in them. The parties must prove they’re serious about supporting Australian business, with the intent to follow through on their promises regardless of the political landscape post-election. A promise not kept does more harm than good.

More importantly, policies that support SMEs and the overall economy must be sold to the public. That’s the job of politicians and the business community.

SMEs are the lifeblood of the Australian economy, and what’s good for SMEs tends to be good for everyone, especially during a domestic housing downturn and an unpredictable global political climate.

By helping the Australian public understand the importance of strong SMEs, the political and policy incentives of politicians become aligned. With everyone paddling in the same direction, it’s much more likely we’ll find a path around those dangerous waters.

Marketlend Academy: The Biggest Mistake An SME Can Make

Listen to CEO and founder of Marketlend, Leo Tyndall, discuss the biggest mistake an SME can make when it comes to its financial health, and why time management and decision making are critical. If you want to read the full transcript please see below.

I think it’s difficult to say it’s a mistake. I think it’s, it’s unfortunate to say a mistake. I think what’s happened is that SMEs don’t have a lot of time to actually make decisions. And the biggest problem they have is that the options for them to pick the right financier are just not in their face, so the mistake they do is not enough due diligence.

Now, is it a mistake or is it just a difficulty? I think it’s more like a difficulty they have in their space that the first thing most SMEs think when you’ve asked them about finance is “The bank.” And then they’ll go to their bank and they could waste a lot of time where they could find they don’t have probably collateral and can’t even get a loan, or you have this thing that they go on the web and they see an SME lender, and they click a few buttons. Go, “Whammo, I’ve got my money.” But they don’t look at the implications and how that affects their business as a whole.

So the biggest problem that I think we have in Australia, which is a very unusual problem in Australia, is that we don’t have a very deep equity market for small SMEs and we don’t have a very deep debt market for SMEs. So, as a result of that, they don’t have the option say like in the US or something similar where they can actually bring on venture capitalists, or they can bring on other funders to help them with the funding. They have to essentially just take what’s right in front of their face, and the problem being what’s in their face is whoever makes the biggest noise. It’s the SME lender that’s charging 40%. He’s the one who’s going to get the biggest, you know, hits because he’s the one that’s in everyone’s face. They’re not doing enough due diligence.

Marketlend’s funding option GreenLend encourages green investment

This week The Fifth Estate is reporting about Marketlend’s new clean energy funding option GreenLend, which has garnered the participation of leading Australian renewable energy company Planet Ark Power. The new funding plan is on track to connect more environmentally conscious investors with green businesses.

Investors are increasingly looking to invest “beyond” their checkbooks and with their consciences, but they can also find it difficult to find and fund businesses that align with their values. In particular, many investors are seeking to invest in solar and renewable assets, while also looking to avoid big banks and high interest rates.

That’s where GreenLend offers a solution since it was designed to accelerate the expansion of solar capacity and other clean energy in Australia. It helps sophisticated and wholesale investors directly fund clean energy SMEs by offering them a special interest rate on loans from Marketlend’s investors.

According to founder and CEO of Marketlend, Leo Tyndall, Marketlend has always taken a long-term view when it comes to financing SMEs.

“We want businesses to thrive long into the future,” he says. In fact, since its launch in 2014, Marketlend has funded over AUD$56 million to Australian SMEs. But GreenLend specifically targets Australia’s energy future by “ensuring today’s energy innovators get the access to capital they need so they can continue addressing one of the world’s most pressing concerns – climate change.”

SMEs can apply for funding on Marketlend’s online lending platform, and those businesses in the clean energy space will be marked with a special badge to help investors identify them. This will be based on criteria that will include supporting SMEs largely or wholly focused on clean energy, sustainable products, recycling and energy efficiency. Once identified as ‘green’, these borrowers receive an attractive interest rate of 8-9 percent while investors in these clean energy businesses will typically earn a return of between 5 percent and 7 percent.

The funding plan’s first borrower, Brisbane-based Planet Ark Power, has received a $500,000 loan from fifty investors through GreenLend. It will be use the money to improve cash flow, trade credit, and working capital. Planet Ark Power’s mission is to help businesses, governments, and individuals reduce their impact on the environment. Executive Director Richard Romanowski explains that the energy provider’s main focus is making renewable energy as efficient and hassle free as possible. The greater the uptake of renewables, he explains, the greater the benefit to the planet.

But in the past financial hurdles had hindered growth plans, which is why Marketlend’s GreenLend can help the company. The funding plan connects Planet Ark Power directly with investors, and helps the company rapidly increase recruitment and installation of more rooftop solar panels across Australia.

“In turn, we’re able to save households and businesses millions of dollars while reducing our carbon footprint – it’s game changing stuff,” Romanowski says.

While Planet Ark Power is one of the first companies to receive funding, Marketlend is uniquely placed to connect more SMEs with needed funding, helping them progress across their growth curve and achieve scale in ways they couldn’t before.

Inadequate regulation of fintech leaves Australian SMEs at risk

By all accounts, Australia is poised to become one of the world leaders in fintech. We’re an incubator for new ideas and experimentation. Despite this, an inadequate regulatory environment and lack of support for small-to-medium enterprises (SMEs) continues to put the fintech industry, and the small business community, at unnecessary risk.

The stakes for Australia’s economy are high. Small businesses, which employ half of the nation’s workforce and make one fifth of its domestic product, remain vulnerable to the loan shark practices of fintech bad guys.

That’s true even with a new voluntary code of lending practice that Fintech Australia recently put in place to self-police albeit not all lenders are even members of the organisation. The code claims to standardise transparency and create a mechanism to resolve disputes, but only six fintech companies have signed on and it has no real teeth.

While the code includes a pledge to lend only to SMEs that have the capacity to repay, there is no mechanism to stop loans to SMEs that have outstanding loans from other fintechs — a practice known as “stacking.” Nor does the code address some lenders’ insistence on repayment by relentless direct debits that can drive SMEs out of business. Finally, it’s not clear whether the code can be enforced or is merely a set of guidelines.

In other words, we’re not signing up because it is not a legitimate attempt to enable responsible lending — it’s an empty gesture for a quick PR hit. As mentioned it does not apply to non-Fintech Australia members. Furthermore, its definition of an SME loan excludes the majority of the lending in the SME arena.

In effect, then, the problems that brought on the code still exist. As an experienced SME lender, we are gobsmacked how anyone can suggest that the majority of SMEs will understand the real cost when a loan is offered on a factor rate (shouldn’t it be as simple as the question, what is the interest rate after all costs?). In fact, reports of ASIC’s recently completed review of one of the most prominent fintech SME lenders are notable for absenting lender’s factor rates from review and thus excluding what is arguably the most problematic and damaging part for SMEs from scrutiny.

While fintechs can still serve startups as an excellent alternative to traditional banks, particularly if they’re small- or medium-sized, some startups will likely still fall prey to unscrupulous practices. We have seen SMEs who have had their cash flow drained by frequent debits they could not afford and literally have to close up shop, and, even more unbelievably, it was accountants and other financial advisors who recommended these kinds of loans for their unsuspecting clients.

So the regulatory environment needs to be strengthened, and Australia needs to provide more education and better support for small businesses. The reality is, it’s easier to start a new business in Australia than it is to get a driver’s license, and that’s not a good thing.

There’s a big difference between having a good business idea, and having the business acumen to get it off the ground. More than half of SMEs close within the first three years, and the most common reason is financial hardship.

There are some simple steps that the government could take to address these problems. It could apply the National Credit Code for Retail to SMEs, so they would come under its protections, at least for loans under A$100,000. These include a bar on extending credit to consumers who are likely to have difficulty making payments. Further, the code of lending practice should be amended to forbid loan stacking and mandatory debits. It could remove prepayment penalties, why should an SME suffer to paying a loan out early. Isn’t this a sign of a well run business?

The government should also support SMEs with a licensing and education. With such a program, new entrepreneurs could have a better understanding of money, marketing, cash flow and lending — including the ability to spot a bad loan a mile off.

Why is this so crucial?

It’s crucial because SMEs serve as the economy’s engine. If too many SMEs go belly up from poor business decisions, including bad loans from shady fintech lenders, it affects a fundamental base of our economy and it hurts Australia’s reputation as a fintech innovator.

Our fintech industry now ranks among the top ten in the world. If we pay attention to the small businesses upon which it is built, Australia can further strengthen its reputation. Everybody wins: The SMEs, which will be less likely to go out of business; the lenders, who will be less likely to lose money on bad risks; and the nation, which will continue to thrive as a world leader in fintech.

Marketlend Academy: what we look for in investors

Watch Marketlend’s Chief Investment Officer, Jane Lehmann, talk about what Marketlend looks for in its investors. The text of her comments appears below if you prefer to read.

Marketlend has a very specific requirement in regards to its investors. Under the Corporations Act, we are required to only engage experienced, sophisticated, wholesale, official investors. So for an experienced investor, that really is someone who can demonstrate that they have, as the name suggests, experience in lending in these types of financial instruments, and truly understand the risks that they’re undertaking when they engage in the platform. Sophisticated is actually a means test related defining feature that you need assets of a 2.5 million. I think the inference there is they also are a more sophisticated and experienced investor.

The institutional investors have a different profile that they tend to be funds. Many of them are offshore. And for them they often have a specific risk profile that they’re interested in and we can customise that for them. We have a pool of loans that we have onboarded and we can work with them to understand what their risk tolerance is where there are risk sectors they’re not comfortable with, where they have an appetite and craft a portfolio for them.

The experienced and sophisticated investors have the opportunity to go on to the platform and make their own assessments. They can look at each loan that is presented and make their own assessment and take a view on whether that is something that appeals to them as an investment opportunity. And that is obviously why you need experienced investors, because they are making a financial decision.

Listen To The Investor Townhall

This past week, Marketlend ran an investor townhall. Transparency is integral to how Marketlend operates. Our investors expect it and we are committed to delivering on this promise. The investor townhall offered a chance to roll up our sleeves and explore issues that matter to the investor community.

We dug down into the mechanics of how we return principal in the event of a problem loan and the integrity of the Marketlend platform generally. There was ample room for Marketlend’s Founder and CEO to field questions and the result was a really engaging and hopefully enlightening look inside the how and why of this aspect of the Marketlend platform. Click above to have a listen.