How to choose the right accountant

Following last week’s post about how an accountant can free you from bookkeeping to focus on running your business, how do you know which accountant to choose once you’ve made the decision?

In this post we list 5 things to consider when choosing the right accountant.

1. Cost

You’ll likely encounter many different cost options because the cost of an accountant varies depending on the specific services you’re seeking. These services may include bookkeeping, tax services, or more complex business accounting tasks. Some accountants charge per hour, while others may request a flat rate per project.

Business Insider reports accounting hourly rates typically fall between $200 and $300 per hour, while a simple business tax return could cost a flat fee of $2,200 to $3,300. You have to consider your budget and decide what specific services you require, and then look for accountants within your budget.

2. Interview

Speak to the accountant you’re considering before you hire. Make sure you understand how they work and what services they specialise in. You may have questions for your accountant as your business grows, so get a feeling for whether the accountant would be easily available to speak to you when you require it. Also look for someone whose goal is to help you manage your cash flow, and not just boost their bottom line.

3. Credentials and references

Look at the credentials of any accounting firm or individual accountant you’re considering. Make sure they’re properly trained and experienced, and don’t forget to ask for references. Just like when hiring an employee, you’re hiring someone to perform a service for you. We recommend speaking with at least two referees before you make your decision. Other ways of securing references can be via social media, review sites or business associations, and you may also consider running a background check.

4. Location

Depending on your situation and the type of business you run, you may want an accountant that you can meet frequently with in person. If that’s the case, seek someone near you or consider whether you can get by with phone calls and video conferencing if the firm is further away. It all depends on your specific needs and preferences, which only you can define.

5. Data and Software

One big benefit of working with accountants is that you don’t have to calculate anything manually – but they don’t do it manually either. Accountants typically use software to keep track of client finances, so it’s a good idea to find out what software they use and whether it’s compatible with your needs. If it’s going to be complicated to get your data in and out of their database, perhaps you need to look elsewhere – discuss what they use and how that would integrate with your business.

Super Cat Converters bucks the banks for better service

While the catalyst to Wayne Chiert starting his automotive supplies business, Super Cat Converters, was an accidental meeting with an American man and his sausage dog, the secret to keeping it running has much less to do with chance.

Super Cat Converters has been using the Marketlend platform since 2017. Wayne says the combination of flexible finance, not needing to sacrifice his house to secure a loan, and working with real people has given him the freedom and support he needs to grow his business.

Conversion catalyst

When Wayne started his business, it was very different to what it is today.

“It’s funny, I didn’t expect to go down this path. A company in the USA approached us to recycle girders. We gave it a go and it really worked out.

“Today, we’re an automotive wholesaler as well as a recycler”, Wayne says. “We offer customers a one-stop service, so they can get everything quickly and efficiently with the service to back it up.”

Wayne is an accountant by trade, and the story of Super Cat Converters’ genesis is probably different to other catalytic converter wholesalers.

“I went to the US to buy a machine and met a very old guy driving a pick-up truck with a sausage dog in the back.

“He said ‘You’re a young man, I’d like to help you out. Here’s a catalog for a major US company, maybe you should give them a call.’ I called them, and they didn’t have any distribution in Australia. That company, Magnaflow, is now our biggest supplier.”

Bucking the banks

Two decades on and the business had expanded into five states with a long list of international clients. During a property sale, Wayne was looking for additional finance but was staring down lengthy delays from the banks.

“We had a property to sell with a long term settlement. We had gone to the banks to ask for a bit of the financing but were looking for alternatives, and we got recommended Marketlend.

“When I first spoke to Leo I said ‘I’ve got a property to sell, I might need a loan to help me out’. Leo went through how Marketlend works and I thought I’d give it a go.

“We met for a few coffees and started with an unsecured $100,000 facility. It’s not like a bank where they just provide you a loan. With Marketlend, they understand your business. You do a video interview that goes on the website, and suddenly you get investors putting bids on your listing. Before you know it, you hit the threshold, you’ve got your loan, settlement’s done and the funds are in your account.”

Wayne says the speed and flexibility of Marketlend made it hard to imagine going back to the banks.

“I think the banks might’ve taken three or four months to do what Marketlend did in two weeks.

“When a bank lends money, they want some kind of property security. With Marketlend, there’s nothing like that. There’s no caveats, so you can have all your properties unencumbered which is a really good thing.”

Dealing with real people

Wayne says that the best thing about Marketlend was, unlike the banks, the Marketlend team took the time understand both him and his business.

“It’s the people you’re dealing with, like Leo and Jeff. You call them on their mobiles, and they’re always available for you. They call you back. If you want to discuss a deal or ask something, the accessibility is incredible.

“It’s so much nicer not dealing with these big scary banks, and instead dealing with people that you know, trust, and have a relationship with.”

Does your SME need a small business website? Yes, here’s why

How many potential customers are you losing because you don’t have a website? How many are moving on to competitors because your small business website looks more at home in the 1990s?

While these questions are impossible to quantify, they are possible rectify.

Recent research by the domain registrar GoDaddy showed 59 percent of Australian small businesses still don’t have a proper website. Forty-four percent of businesses surveyed believed their business was too small to justify investing in a website, and the vast majority of businesses surveyed said they use social media sites to communicate with customers.

Despite websites having a higher barrier for entry than a social media account, there are number of compelling reasons to make the investment. According to the same survey, 61 per cent of business owners said their websites had a significant impact on their businesses, contributing up to 25 per cent growth.

Here are five other reasons you need a business website:

- Another marketing avenue: A company website is another place where you can showcase your goods and services. The more, the merrier.

- Credibility: When a customer is appraising your business, they may believe your operation is less reputable if they cannot find a corresponding website.

- Misunderstanding: You may be missing out on customers who believe you are out of business if they cannot find a website or if it appears outdated.

- Security: Some customers feel more comfortable shopping for goods or services through a secure company website instead of external services.

- Data: Not having a website, or not having one properly optimised for collecting customer information, means you’re missing out on valuable data that you can use to boost sales.

For those who do have a website, but have not updated it in some time, here are the key characteristics consumers look for in a strong, modern company website:

- Purpose and user experience: Make sure your company website reflects the point of your business. If you’re selling a good or a service, make sure that this is immediately clear on your homepage, and that your goods and services are clearly showcased, explained, and easy to find. Also ensure your customers’ experience when navigating the website is simple and intuitive.

- Domain: Make sure you have a professional, easy to remember domain name.

- Security: If customers are given the ability to log in and can make purchases directly from your site, make sure your customers’ data is secure via features like password protection and encryption.

- Reliability: Include important sections such as “Contact Us”, “About Us”, and “Terms and Conditions” pages. Customers may look for these sections to determine your reliability.

- Data collection: Don’t forget to include a system for collecting customer email addresses and other information that will help you target them for repeat sales, special offers, or to adjust your products based on your customer’s interests.

Leaving the Banks Behind: How Planet Ark Power made solar profitable with Marketlend

Upfront costs and unconventional financials have held back the expansion of businesses transforming our energy markets and introducing new ways of delivering electricity.

That’s what happened to Planet Ark Power, an engineering organisation which combines modern PV solar panels and batteries with AI powered software to ramp production up or down based on demand from the electricity grid. With a system that is cash flow positive from day one, Planet Ark Power installations help businesses turn energy from a liability into a revenue stream, as well as providing energy security.

But not too long ago, Planet Ark Power struggled to get the funding they needed to grow.

“5 Months of Hell” – The role of the right finance

Rapid growth brings rapid change, and Planet Ark Power needed a line of credit to cover the cost of those changes. But Executive Director Richard Romanowski says his experience with getting finance from the banks was less than ideal.

“The bank put us through five months of hell, then said ‘go make your sales targets for the year and come back to us’. The banks will only give you money AFTER you’re successful, with no regard for how much energy it takes.

“That’s when Marketlend came to the rescue. They asked us to explain what we were doing and our business prospects. When they understood our challenge, they said ‘this is a great opportunity’.”

By looking solely at past numbers, investors can easily miss high value opportunities like Planet Ark Power. The Marketlend platform makes up for what’s lacking in the traditional lending model by providing investors both a quantitative and qualitative assessment of each company.

In doing so, small to medium enterprises have more flexible access to fast finance, allowing them to take advantage of growth opportunities in their sector.

How Marketlend made growth simple

Through the Marketlend platform, Planet Ark Power borrowed $500,000 from 50 lenders, which Romanowski says has been a game changer for the business.

“The cost of client acquisition is huge. We’ve gone from $30,000 sales to $10 million sales, and each one is a massive learning curve – building new systems, new sales approaches and so on.

“I have a 5-star contract but I have to wait 60 days to get paid. With a customer base growing and changing so fast, I need cash flow to handle it.”

No more missed opportunities

Marketlend puts sophisticated investors in touch with high potential opportunities that fall through the cracks of traditional lenders. It avoids the many pitfalls of a peer-to-peer lender, because it is a vetted, thoroughly transparent lending platform.

“Marketlend actually cares about your business. They really want to know what you are doing,” Romanowski says.

“They take a bit of a punt with you – not in a lender-of-last-resort way, but in a way that actually understands the risk and reward.

“We now have a $500,000 line of credit and are looking to increase it. When we first went to Marketlend we had 25 staff, today we have 35. Not only that, the size of the projects are growing fast.

“Because they really understand your business, they can unlock the opportunity.”

Marketlend Academy: Marketlend performance for 2018

Each year it’s worth looking back to take stock, and we’ve been doing some of that at Marketlend – we’re happy to see that Marketlend performance in 2018 was as strong as it has ever been. Watch Marketlend CEO Leo Tyndall outline what it was that made 2018 a strong year for Marketlend’s investors and borrowers, and what’s making him excited about the future of peer to peer lending. You can also read the transcript below.

Video Transcription:

We had a great year. So from a volume point of view we’ve been very successfully growing our book. At the same time, from a risk point of view, we’ve been able to ensure that our book has grown, but not increased the negative effects of such a growth factor. So what we’ve seen is our default rates have actually reduced, it’s gone down from the 4.6% that we had for the year down to around 2-2.2%. But what we’ve also seen is we’ve been able to control the product that we produce and that means that investors have been able to get a great return. So the average return from a net point of view has been 10.2%. What we’ve seen is that we’ve been able to grow, and as I mentioned in other videos, that we’ve seen a growth of our book double compared to last year, so we’re up to $61 million funded.

We still look at December being a strong month as well, but what we’re seeing very much is also an increased focus of due diligence and implementation of some of the measures we brought in early in the year. We send out an external accountant if the exposure’s greater than $250,000, which has helped us significantly to really get to know our client, and then spending a lot of time interacting with our client post settlement. So we’ve put on settlement clerks, you could put it, so that they can interact with them post settlement so that we can increase the utilisation as well of the actual portfolio. So it’s been a great year for us.

As far as staff goes we’ve now got a total of about 35 people. In Australia we have around 15 to 16. I count that number because we only just put on two new people again today. So we’re continuously growing the actual support staff. We’ve also got the Philippines team which is a total of 14 people, and then we have developers all over the world. So it’s been a great year for us.

Marketlend Academy: How much should a small business spend on marketing?

Selling yourself is a part of every business, and marketing is the way it’s done at scale. But how much should a small business spend on marketing?

Like any question worth asking, the answer depends on your situation. Read on for some insight into what businesses are spending on marketing today, and what you need to think about before setting your own marketing spend.

Define your needs

What you want to achieve goes a long way to determining your budget. Your needs are different from other companies and will change over time. You may want to:

– Grow fast

– Grow sustainably

– Build brand awareness

– Maintain an established presence

These are all very different goals, with different associated costs. If you’re just starting out, every company needs a cohesive brand and a functional, professional website. Beyond that, your needs are completely custom.

With that caveat, there are some standards you can use to set your expectations.

How much should a small business spend on marketing?

Marketing budgets are normally measured as a percent of company revenues. To get a dollar amount from the percentages below, multiple them by a firm’s gross revenue.

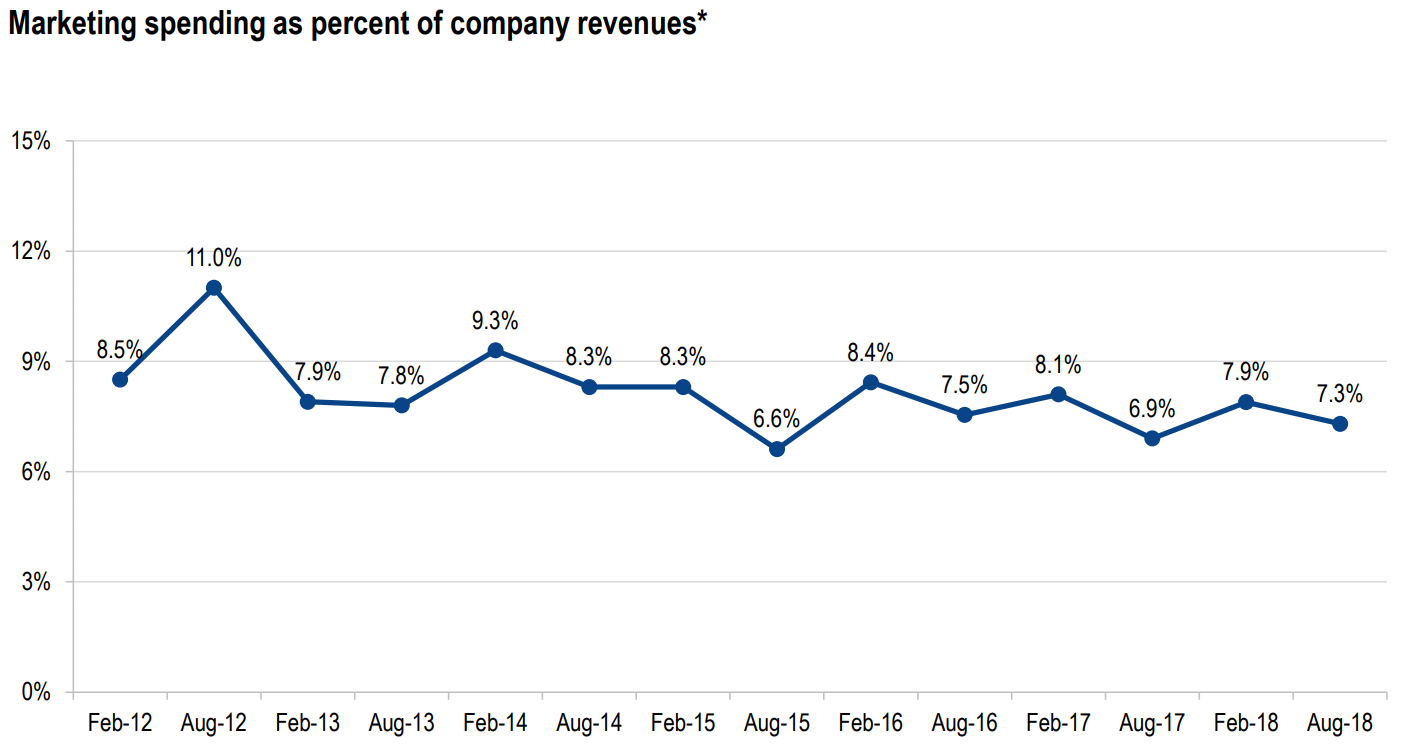

The August 2018 CMO Survey from the American Marketing Association found an average marketing spend of 7.3% of company revenues from 324 respondents across the US.

The chart below shows this is lower than recent years, but still within a typical range of 7-9% of revenue (source page 26).

Marketing for startups vs established firms

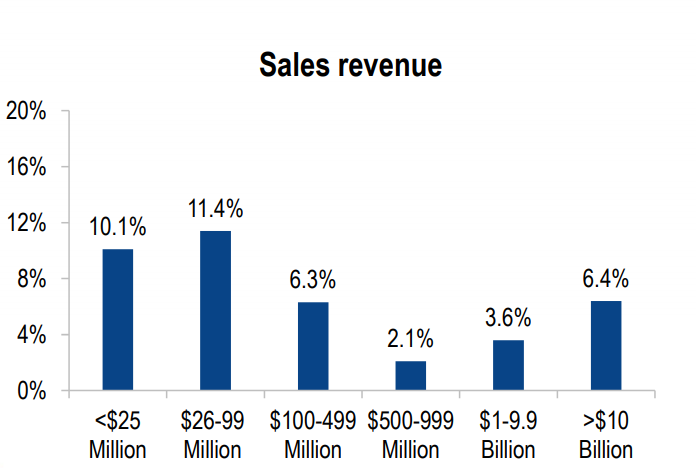

The report calculated average marketing spend by company size, as seen below (source page 27). Generally, smaller firms spend more on marketing than larger companies.

The first step of marketing is brand awareness, so smaller businesses without established brands are wise to spend more on marketing. Established brands can get away with a more efficient budget.

Ryan Flannagan of Nuance Media writes startups should expect to spend 12-20% of gross revenue on marketing, while noting a larger firm may only spend 6-12% of gross revenue on their marketing budget.

When the rules don’t apply

Knowing the rules helps you know when to ignore them, and a standard marketing budget won’t suit every company.

The CMO Survey breaks down marketing budgets as a percent of firm revenues by sector, below (source page 27).

Clearly there are situations where a big traditional marketing spend isn’t as useful. B2B services like mining, manufacturing, and professional services for instance typically rely on sales teams to attract new clients (with sales rarely included in marketing budgets).

Avoiding over-marketing

You can over-spend on marketing. First, there’s the opportunity cost of a high marketing budget that may be better spent on product or business development.

But there’s also the risk of growing too fast. If your marketing is too effective, you may face more growth than you can handle. That can cause serious cash flow problems that undermine other parts of your business, potentially sending you out of business.

Avoiding this isn’t difficult. First, don’t borrow more than what you need for the growth you can handle. If you’re using Marketlend to access flexible, peer-to-peer finance, don’t over leverage yourself. Make your repayments and you can always extend your line of credit later.

If you do have cash flow issues as you grow, a service like UnLock can provide extended payment terms to supercharge your cash flow, like a corporate version of buy-now-pay-later.

Pay it smart

The key element when setting a marketing budget is to be deliberate. Approach your marketing spend with a critical mind and a clear vision of what you want to achieve, and you’ll be miles ahead of the competition already.

Marketlend Academy: Increasing borrower interaction to make better investment opportunities

Despite being a fintech, we know the importance of face-to-face interaction with real people. In the lending business, that sometimes means visiting an SME in person and getting to know their business from the inside out.

Below Marketlend CEO Leo Tyndall describes the importance of borrower interaction, and why it’s such an important part of Marketlend’s approach with large exposures. You can also read the video transcript below.

Video Transcript:

The changes that we did at the beginning of the year was to actually make sure that we have a lot more interaction with the borrower post settlement. Some of those changes included that for exposures over $250,000, we actually have an independent accountant who actually goes to their premises, kicks the tires, reviews their balance sheet, looks at all the other factors that could be of risk for the underlying investor.

One of the things that we’ve seen through our portfolio over four years now has been that some of the risk elements that are not as easy to see from just documents and the like, is exactly if there’s personal issues or if there’s something that we should be concerned about. For a classic example, one of our borrowers unfortunately passed away. That caused a stress on the book. Had we sent out the external accountant he would have given an idea that there wasn’t possibly enough succession in that position. Fortunately for us the insurer paid out and we were able to cover our exposure for all the investors, but it was something that … we would’ve been able to have a much better idea had we had someone go out, sit with them. It also from a borrower experience actually helps significantly as well. They get to know them, in a way it helps them understand their own risk.

So we implemented that at the beginning of the year and that’s been very successful. And that accountant is a chartered accountant. He goes out there, he does do a review, he does the report internally for us. We are not at the stage where we will be producing that report externally, but down the track we may be looking at a summarised report for that.

But the important part there is whilst we’re a fintech, we still are someone who actually does touch and go and see the investor and have a relationship with them. And I think one of the things that, if you would say over the four years what we’ve seen significant changes in, has been sure, when you’re lending the small amounts of $25,000-$30,000 you may get away with doing it all online and not actually meeting the client, but when you’re starting to invest significant money with them it’s very important to actually get to know your client. And from also an anti-money laundering point of view it helps us significantly as well.

Detecting cyber fraud as a small business owner

As a small business owner, you may have already had an experience with a scam targeting your business. It’s reported that Australian small businesses lost more than $2.3 million from cyber attacks in the first half of 2018, with nearly 18 per cent of small-to-medium-sized businesses in Australia having been impacted by a cyber scam.

While this seems like it would only affect you, it can also impact your customers. For example, hackers can “spoof” your business email account so their emails look like they belong to you. They can then contact your customers and request payments be made to a different account instead of your own. One Australian business recently reported losing $300,000 to such a scam.

In another version of this attack, scammers can intercept your correspondence with suppliers, and then pretend to be the supplier in order to get you to pay them instead. Other popular tactics include ransomware attacks in which your data is encrypted and held hostage until you pay the scammers a ransom. Thieves being thieves, you can never be sure if you’ll receive your data back even if you pay.

With so many ways you could be targeted, detecting cyber fraud is a top priority. To help you, here are several tips we suggest you follow to recognise and prevent a potential scam.

1. Never click on any links or attachments in an email unless you know the source and can verify its legitimacy. Poor spelling and grammar usually gives away fake emails.

2. Install anti-phishing software.

3. Never wire money to anyone you don’t know in person. Asking for wired money via services like Western Union is a very common scam.

4. Never fall victim to an urgent transaction. Typically, cyber attackers want to get your money as soon as possible so they can disappear. Confirm the transaction with your usual contact if things seem suspicious.

5. Make sure you keep back-ups of all your data. This will enable you to return to business as usual in the event you fall victim to ransomware without having to pay the attackers.

6. Check the URL of any website you’re asked to access, especially ones where you have to enter sensitive information, to make sure the website is legitimate. A fake URL may look similar but can have spelling errors. If it is hyperlinked, you can check the website by hovering your mouse over the link. Otherwise, type the address in the search bar yourself if it’s a website you know, such as an online banking portal.

7. Make sure that any financial transaction you engage in online requires you to enter your details only after the URL changes from “http” to “https”, this means the connection is secure – all Australian bank log-in pages are https.

8. Limit who in your business has access to sensitive financial details to those who absolutely require it.

9. Trust your gut. If something feels odd, or you see an offer that seems too good to be true, then it probably is.

10. Report suspicious activity. Most Australian banks, telcos, and energy providers – the industries most frequently impersonated by scammers – have sections on their websites where you can report a scam. They also publish details of current illegitimate activity.

Marketlend Academy: 2019 Outlook – The big challenges for 2019

2019 looks like another good year for Marketlend, which is great news for you. A strong year for Marketlend means even more flexible finance for SMEs to grow, and more great opportunities for investors.

Watch Marketlend CEO Leo Tyndall’s 2019 outlook, what he’s excited about, and what he sees as the biggest challenges in the year ahead. Or, read the transcript below.

Video Transcript:

We’re looking at quite a very positive year ahead. We’ve recently engaged two new sales team who are ex American Express and we’ve seen a significant pickup in our origination volumes in the last year. So we see that in the last month, in November, we did 5.2 million and we see that we’re possibly looking at similar numbers or even doubling those numbers going forward.

With the avalanche of these new products we’ve brought out, essentially UnLock as well as GreenLend, we see a bit of energy there coming back from an investor base as well as from the borrower base. And so what we see is from that side, a very exciting year. From the risk side we have added additional measures to protect our position, or the investor’s position, and so where we see with that is that we see a continued good performance from the book and also seeing that our clients are actually gonna grow with it.

As far as the economy goes, there are some stresses that we are cognisant of and concerned about, especially the construction industry as well as the possible retail industry as the continual issue with the fact of the online businesses growing so well and the retail business, sort of, lease holds being a bit of a struggle. And so what we are focusing is on making sure that we try to diversify away from that as much as possible, or at least when we see those opportunities we ensure that we actually have additional protections for the underlying investors.

Marketlend Academy: Tips to pay off business debt

While some debt is necessary to fund a business, if you’ve ever found yourself turning to a personal credit card to stay afloat… it’s time to stop for a moment and consider your options.

Here’s a sobering statistic: Last year, a survey of 1,200 Australian SMEs showed about two thirds of small business owners rely on credit card debt to maintain cash flow in their business. Just two years earlier, the Australian Bureau of Statistics found only a third of SMEs would use credit cards to maintain cash flow.

That means the number of businesses turning to credit cards to keep their businesses afloat has doubled in two years.

While there’s a certain convenience to using the credit card, the ensuing interest rates can put a business under even more financial pressure. Instead, here are a few tips to smooth out cash flow, and start to pay off business debt in your firm.

- Are your costs too high?

Reevaluate your regular expenses. Are you paying too much for supplies or materials? Research new suppliers and see if you can get similar materials elsewhere for less.

You could also reduce your office space and sell off equipment you don’t need or no longer use, or look into reducing your energy consumption.

This will result in savings you can put toward reducing your debt, or for maintaining cash flow in lieu of entering into even more debt.

- Can you buy now, pay later?

When looking at supplies and materials, have you considered services like Marketlend UnLock? Launched late last year, UnLock is similar to consumer ‘buy now, pay later’ models like Afterpay, except it is designed for small businesses.

In effect, Marketlend pays the supplier upfront for the materials, then gives your SME extended credit terms to pay the amount back – typically 90 days instead of the usual 30-day time frame.

This longer credit term allows businesses more time to repay, thereby smoothing out cash flow.

- Can you prioritise paying off your debt?

If you’re going to owe money, then you should know how much you owe and to whom. If you’re accumulating so much debt that it’s becoming challenging to keep track of what payments you must make every month, it’s time to take stock of your debt in order to prioritise your payments. Generally, when looking at loans it’s best to pay off those with the highest interest rate first.

Also consider consolidating loans if possible. Not only are consolidated loans easier to manage, as there are less people to pay, but you can typically find a lower interest rate – depending on the circumstances.

Start Today

This is by no means an exhaustive list, butit’s the three best places to start. If the debt your business carries is slowing you down, the best thing to do is take steps to pay it down today. Even if those steps are small at first, they’ll compound into giant leaps over time.