Super Cat Converters bucks the banks for better service

Bucking the banks

Two decades on and the business had expanded into five states with a long list of international clients. During a property sale, Wayne was looking for additional finance but was staring down lengthy delays from the banks. “We had a property to sell with a long term settlement. We had gone to the banks to ask for a bit of the financing but were looking for alternatives, and we got recommended Marketlend. “When I first spoke to Leo I said ‘I’ve got a property to sell, I might need a loan to help me out’. Leo went through how Marketlend works and I thought I’d give it a go. “We met for a few coffees and started with an unsecured $100,000 facility. It’s not like a bank where they just provide you a loan. With Marketlend, they understand your business. You do a video interview that goes on the website, and suddenly you get investors putting bids on your listing. Before you know it, you hit the threshold, you’ve got your loan, settlement’s done and the funds are in your account.” Wayne says the speed and flexibility of Marketlend made it hard to imagine going back to the banks. “I think the banks might’ve taken three or four months to do what Marketlend did in two weeks. “When a bank lends money, they want some kind of property security. With Marketlend, there’s nothing like that. There’s no caveats, so you can have all your properties unencumbered which is a really good thing.”Dealing with real people

Wayne says that the best thing about Marketlend was, unlike the banks, the Marketlend team took the time understand both him and his business. “It’s the people you’re dealing with, like Leo and Jeff. You call them on their mobiles, and they’re always available for you. They call you back. If you want to discuss a deal or ask something, the accessibility is incredible. “It’s so much nicer not dealing with these big scary banks, and instead dealing with people that you know, trust, and have a relationship with.”Does your SME need a small business website? Yes, here’s why

- Another marketing avenue: A company website is another place where you can showcase your goods and services. The more, the merrier.

- Credibility: When a customer is appraising your business, they may believe your operation is less reputable if they cannot find a corresponding website.

- Misunderstanding: You may be missing out on customers who believe you are out of business if they cannot find a website or if it appears outdated.

- Security: Some customers feel more comfortable shopping for goods or services through a secure company website instead of external services.

- Data: Not having a website, or not having one properly optimised for collecting customer information, means you’re missing out on valuable data that you can use to boost sales.

- Purpose and user experience: Make sure your company website reflects the point of your business. If you’re selling a good or a service, make sure that this is immediately clear on your homepage, and that your goods and services are clearly showcased, explained, and easy to find. Also ensure your customers’ experience when navigating the website is simple and intuitive.

- Domain: Make sure you have a professional, easy to remember domain name.

- Security: If customers are given the ability to log in and can make purchases directly from your site, make sure your customers’ data is secure via features like password protection and encryption.

- Reliability: Include important sections such as “Contact Us”, “About Us”, and “Terms and Conditions” pages. Customers may look for these sections to determine your reliability.

- Data collection: Don’t forget to include a system for collecting customer email addresses and other information that will help you target them for repeat sales, special offers, or to adjust your products based on your customer’s interests.

Leaving the Banks Behind: How Planet Ark Power made solar profitable with Marketlend

“5 Months of Hell” – The role of the right finance

Rapid growth brings rapid change, and Planet Ark Power needed a line of credit to cover the cost of those changes. But Executive Director Richard Romanowski says his experience with getting finance from the banks was less than ideal. “The bank put us through five months of hell, then said ‘go make your sales targets for the year and come back to us’. The banks will only give you money AFTER you’re successful, with no regard for how much energy it takes. “That’s when Marketlend came to the rescue. They asked us to explain what we were doing and our business prospects. When they understood our challenge, they said ‘this is a great opportunity’.” By looking solely at past numbers, investors can easily miss high value opportunities like Planet Ark Power. The Marketlend platform makes up for what’s lacking in the traditional lending model by providing investors both a quantitative and qualitative assessment of each company. In doing so, small to medium enterprises have more flexible access to fast finance, allowing them to take advantage of growth opportunities in their sector.How Marketlend made growth simple

Through the Marketlend platform, Planet Ark Power borrowed $500,000 from 50 lenders, which Romanowski says has been a game changer for the business. “The cost of client acquisition is huge. We’ve gone from $30,000 sales to $10 million sales, and each one is a massive learning curve – building new systems, new sales approaches and so on. “I have a 5-star contract but I have to wait 60 days to get paid. With a customer base growing and changing so fast, I need cash flow to handle it.”No more missed opportunities

Marketlend puts sophisticated investors in touch with high potential opportunities that fall through the cracks of traditional lenders. It avoids the many pitfalls of a peer-to-peer lender, because it is a vetted, thoroughly transparent lending platform. “Marketlend actually cares about your business. They really want to know what you are doing,” Romanowski says. “They take a bit of a punt with you – not in a lender-of-last-resort way, but in a way that actually understands the risk and reward. “We now have a $500,000 line of credit and are looking to increase it. When we first went to Marketlend we had 25 staff, today we have 35. Not only that, the size of the projects are growing fast. “Because they really understand your business, they can unlock the opportunity.”Marketlend Academy: Marketlend performance for 2018

Marketlend Academy: How much should a small business spend on marketing?

Define your needs

What you want to achieve goes a long way to determining your budget. Your needs are different from other companies and will change over time. You may want to: – Grow fast – Grow sustainably – Build brand awareness – Maintain an established presence These are all very different goals, with different associated costs. If you’re just starting out, every company needs a cohesive brand and a functional, professional website. Beyond that, your needs are completely custom. With that caveat, there are some standards you can use to set your expectations.How much should a small business spend on marketing?

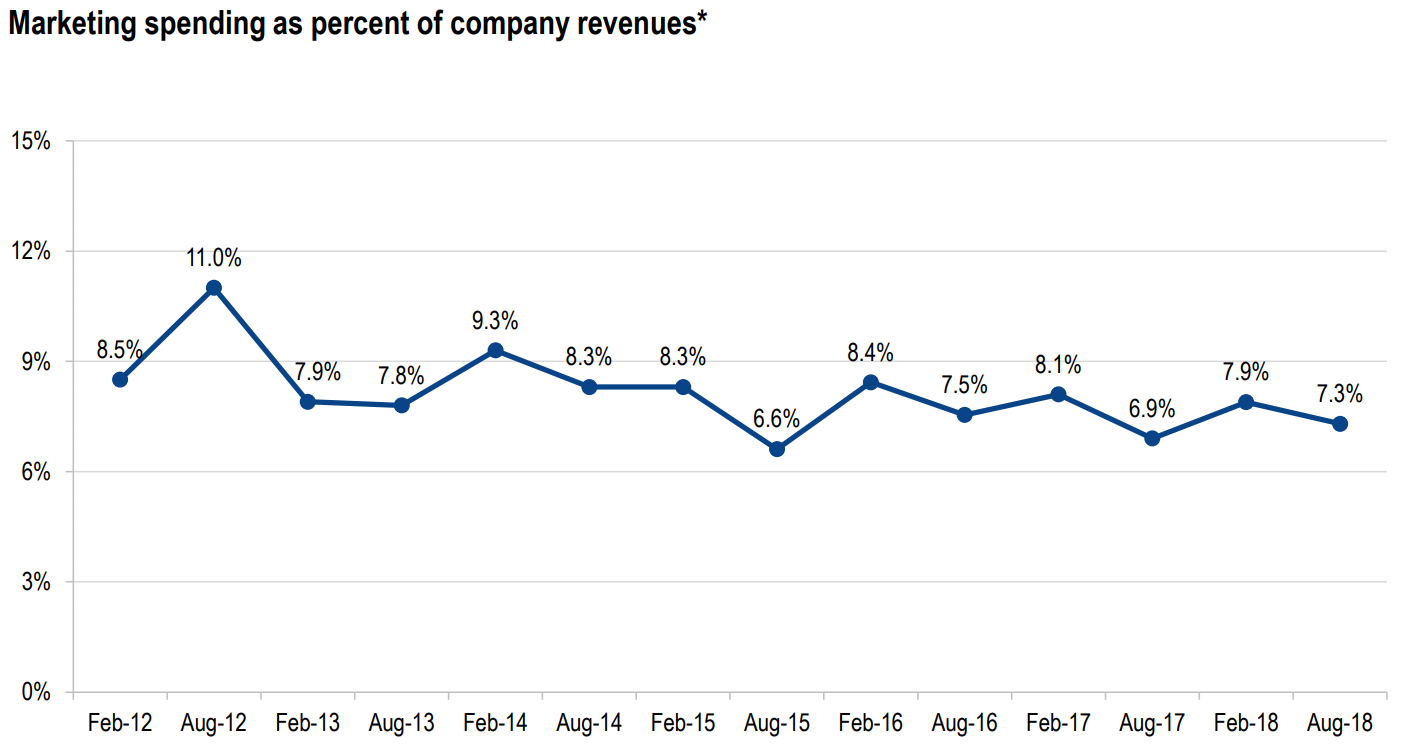

Marketing budgets are normally measured as a percent of company revenues. To get a dollar amount from the percentages below, multiple them by a firm’s gross revenue. The August 2018 CMO Survey from the American Marketing Association found an average marketing spend of 7.3% of company revenues from 324 respondents across the US. The chart below shows this is lower than recent years, but still within a typical range of 7-9% of revenue (source page 26).

Marketing for startups vs established firms

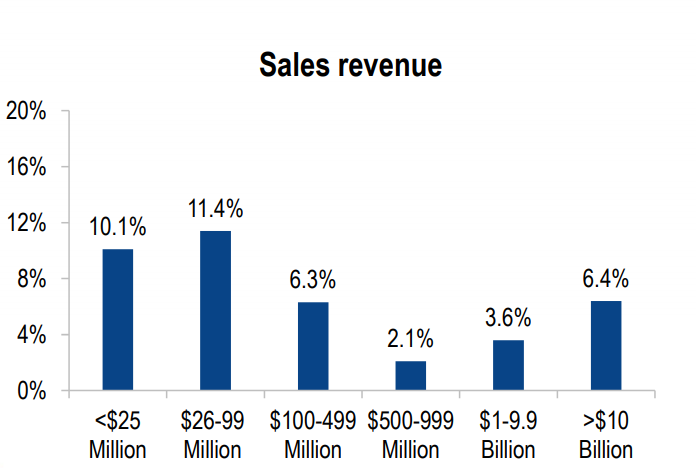

The report calculated average marketing spend by company size, as seen below (source page 27). Generally, smaller firms spend more on marketing than larger companies. The first step of marketing is brand awareness, so smaller businesses without established brands are wise to spend more on marketing. Established brands can get away with a more efficient budget.

Ryan Flannagan of Nuance Media writes startups should expect to spend 12-20% of gross revenue on marketing, while noting a larger firm may only spend 6-12% of gross revenue on their marketing budget.

The first step of marketing is brand awareness, so smaller businesses without established brands are wise to spend more on marketing. Established brands can get away with a more efficient budget.

Ryan Flannagan of Nuance Media writes startups should expect to spend 12-20% of gross revenue on marketing, while noting a larger firm may only spend 6-12% of gross revenue on their marketing budget.

When the rules don’t apply

Knowing the rules helps you know when to ignore them, and a standard marketing budget won’t suit every company. The CMO Survey breaks down marketing budgets as a percent of firm revenues by sector, below (source page 27). Clearly there are situations where a big traditional marketing spend isn’t as useful. B2B services like mining, manufacturing, and professional services for instance typically rely on sales teams to attract new clients (with sales rarely included in marketing budgets).

Clearly there are situations where a big traditional marketing spend isn’t as useful. B2B services like mining, manufacturing, and professional services for instance typically rely on sales teams to attract new clients (with sales rarely included in marketing budgets).

Avoiding over-marketing

You can over-spend on marketing. First, there’s the opportunity cost of a high marketing budget that may be better spent on product or business development. But there’s also the risk of growing too fast. If your marketing is too effective, you may face more growth than you can handle. That can cause serious cash flow problems that undermine other parts of your business, potentially sending you out of business. Avoiding this isn’t difficult. First, don’t borrow more than what you need for the growth you can handle. If you’re using Marketlend to access flexible, peer-to-peer finance, don’t over leverage yourself. Make your repayments and you can always extend your line of credit later. If you do have cash flow issues as you grow, a service like UnLock can provide extended payment terms to supercharge your cash flow, like a corporate version of buy-now-pay-later.Pay it smart

The key element when setting a marketing budget is to be deliberate. Approach your marketing spend with a critical mind and a clear vision of what you want to achieve, and you’ll be miles ahead of the competition already.Marketlend Academy: Increasing borrower interaction to make better investment opportunities

Detecting cyber fraud as a small business owner

Marketlend Academy: 2019 Outlook – The big challenges for 2019

Marketlend Academy: Tips to pay off business debt

- Are your costs too high?

- Can you buy now, pay later?

- Can you prioritise paying off your debt?

Listing

How to choose the right accountant

Following last week’s post about how an accountant can free you from bookkeeping to focus on running your business, how do you know which accountant to choose once you’ve made the decision?

In this post we list 5 things to consider when choosing the right accountant.

1. Cost

You’ll likely encounter many different cost options because the cost of an accountant varies depending on the specific services you’re seeking. These services may include bookkeeping, tax services, or more complex business accounting tasks. Some accountants charge per hour, while others may request a flat rate per project.

Business Insider reports accounting hourly rates typically fall between $200 and $300 per hour, while a simple business tax return could cost a flat fee of $2,200 to $3,300. You have to consider your budget and decide what specific services you require, and then look for accountants within your budget.

2. Interview

Speak to the accountant you’re considering before you hire. Make sure you understand how they work and what services they specialise in. You may have questions for your accountant as your business grows, so get a feeling for whether the accountant would be easily available to speak to you when you require it. Also look for someone whose goal is to help you manage your cash flow, and not just boost their bottom line.

3. Credentials and references

Look at the credentials of any accounting firm or individual accountant you’re considering. Make sure they’re properly trained and experienced, and don’t forget to ask for references. Just like when hiring an employee, you’re hiring someone to perform a service for you. We recommend speaking with at least two referees before you make your decision. Other ways of securing references can be via social media, review sites or business associations, and you may also consider running a background check.

4. Location

Depending on your situation and the type of business you run, you may want an accountant that you can meet frequently with in person. If that’s the case, seek someone near you or consider whether you can get by with phone calls and video conferencing if the firm is further away. It all depends on your specific needs and preferences, which only you can define.

5. Data and Software

One big benefit of working with accountants is that you don’t have to calculate anything manually – but they don’t do it manually either. Accountants typically use software to keep track of client finances, so it’s a good idea to find out what software they use and whether it’s compatible with your needs. If it’s going to be complicated to get your data in and out of their database, perhaps you need to look elsewhere – discuss what they use and how that would integrate with your business.