Category Archives: For Investors

Marketlend Academy: what we look for in investors

Watch Marketlend’s Chief Investment Officer, Jane Lehmann, talk about what Marketlend looks for in its investors. The text of her comments appears below if you prefer to read.

Marketlend has a very specific requirement in regards to its investors. Under the Corporations Act, we are required to only engage experienced, sophisticated, wholesale, official investors. So for an experienced investor, that really is someone who can demonstrate that they have, as the name suggests, experience in lending in these types of financial instruments, and truly understand the risks that they’re undertaking when they engage in the platform. Sophisticated is actually a means test related defining feature that you need assets of a 2.5 million. I think the inference there is they also are a more sophisticated and experienced investor.

The institutional investors have a different profile that they tend to be funds. Many of them are offshore. And for them they often have a specific risk profile that they’re interested in and we can customise that for them. We have a pool of loans that we have onboarded and we can work with them to understand what their risk tolerance is where there are risk sectors they’re not comfortable with, where they have an appetite and craft a portfolio for them.

The experienced and sophisticated investors have the opportunity to go on to the platform and make their own assessments. They can look at each loan that is presented and make their own assessment and take a view on whether that is something that appeals to them as an investment opportunity. And that is obviously why you need experienced investors, because they are making a financial decision.

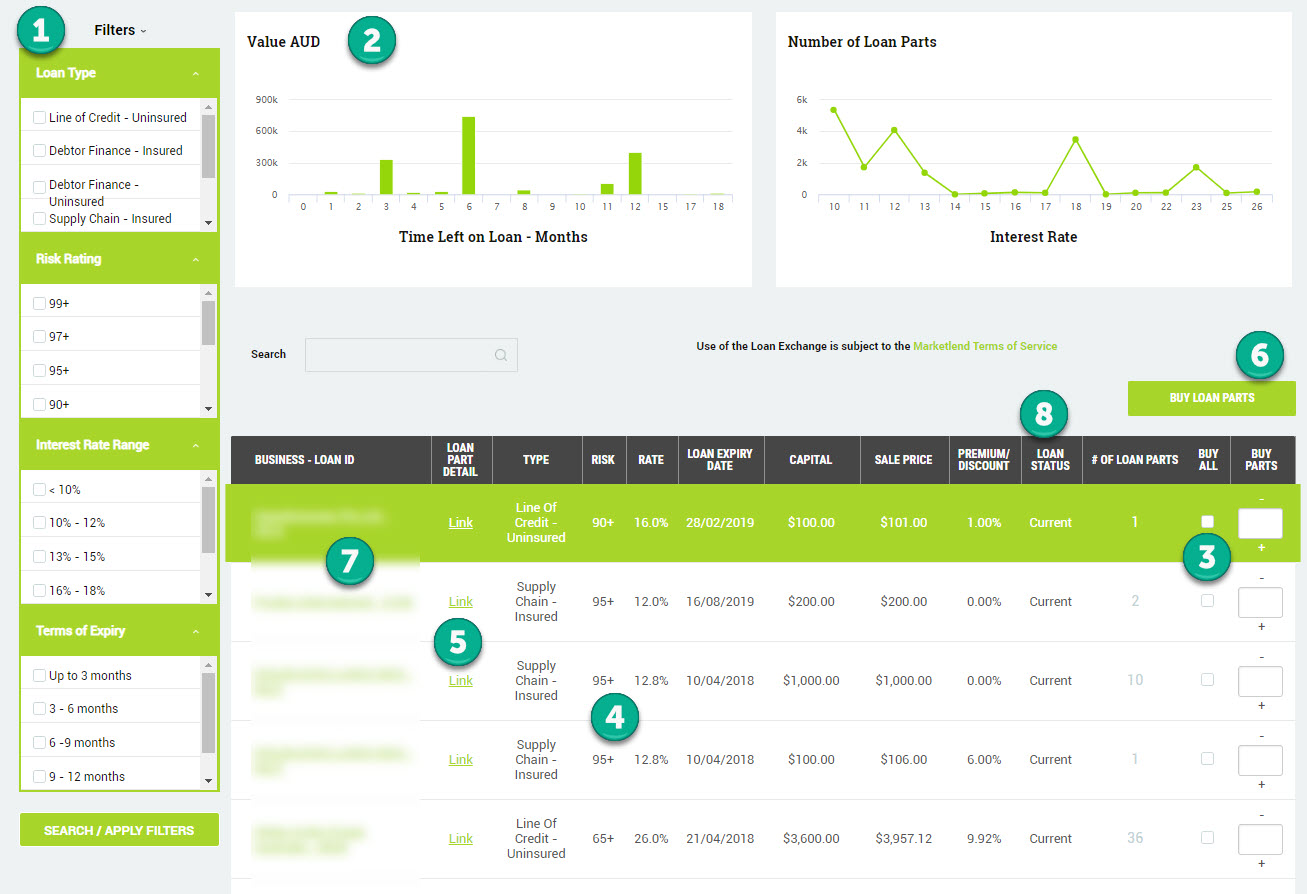

Welcome to the new and improved Marketlend Loan Exchange (Beta)

After ongoing investor testing and community engagement, we’ve created a new user experience built for your needs, the Marketlend Loan Exchange (Beta).

Making the most of Loan Exchange:

When you access the new Loan Exchange you will notice a number of key differences to the existing Exchange.

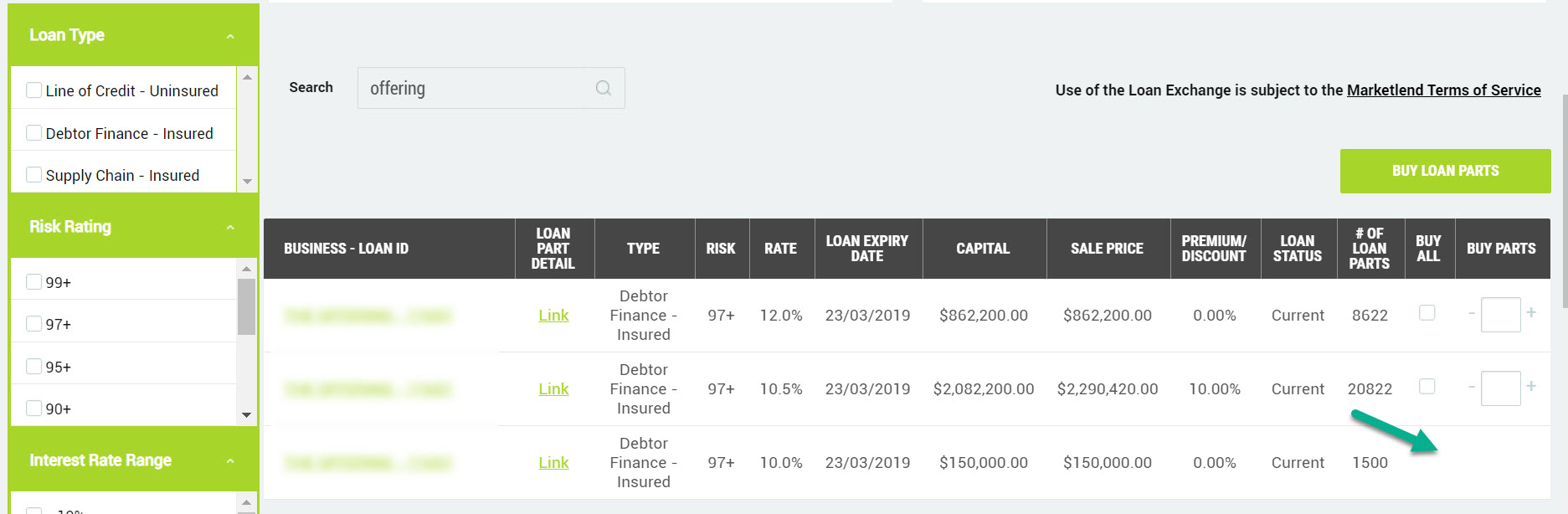

1.We’ve added some Filters to allow you to more easily select loan parts for sale that meet your criteria (depending on the device you are using and the size of your screen the filters will either appear at the side or in a drop down at top of exchange list).

2.We’ve added some graphs to show the make-up of available loan parts on the exchange. The graphs are responsive to changes in the Filters.

3.You can now choose to Buy All parts or a specific number of available parts without needing to view individual parts.

4.Loan Parts for sale are group by Loan/Interest Rate/Premium-Discount value.

5.You can still view all individual loan parts for sale by clicking on the Loan Part Detail Link.

6.Whichever option you choose – Loan Parts are bought by clicking the BUY LOAN PARTS button at the top or bottom of the list.

7.You can view Original loan details and updated Commentary by clicking on the Loan ID link.

8.We’ve added a column to indicate the Status of the loan – showing whether the loan is Current or is in Arrears.

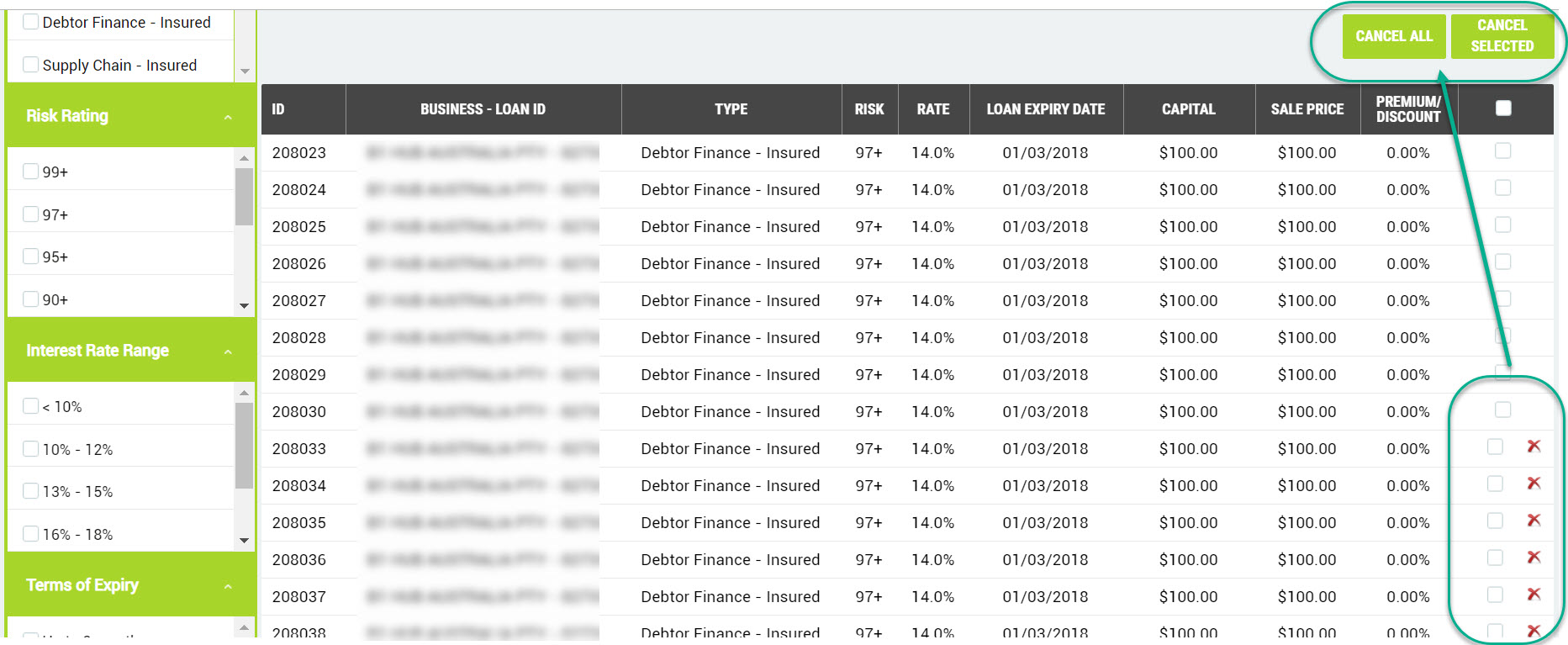

Cancelling Loan Part sales

If you need to cancel a Loan Part that has been put on the Loan Exchange for sale you can still do this from the Loan Exchange page.

If you own any of the Loan Parts for sale for a particular Loan you will see that the option to select Loan Parts to buy is not available.

To cancel any Loan Parts you just need to click on the Link to the loan part details. You can then choose which loan parts sales to cancel or select to Cancel All.

Marketlend Academy: Is Social Media Marketing Worth It?

Is social media marketing like using Facebook and Twitter still worth it? That’s a question many small businesses might be asking these days, considering these trends:

Globally, Twitter is reported to have lost 1 million monthly active users in the second quarter of 2018, while Facebook is expected to lose as many as 2.2 million users by 2022. In Australia as many as 1.8 million Facebook users have reportedly deleted their accounts. All this comes in the wake of the Facebook data privacy furor, which left users wary of social media.

How should this affect your use of social media in marketing your business? It’s more challenging, but still valuable, if you are mindful of these guidelines:

Have a strategic plan

Posting on any social network without a plan or understanding of what you want to achieve will get you nowhere. Decide on your goals and think about how social media can help you achieve them. Define your audience. Otherwise you’ll never break through all the noise, or reach the users that are likely to engage with your brand. Do your research, and keep in mind that the way you need to approach social media marketing may different for each social network.

Post engaging content

Yes, it’s harder to get noticed. But you won’t be noticed at all if you don’t take the time to plan great content that stands out. The same tricks of the trade still stand. You can always pay to advertise branded posts, but this doesn’t replace looking for ways to engage directly with users while promoting your brand, or posting something that helps you make an emotional connection with your intended audience. Offer information or advice that they can’t get anywhere else. You can also run contests, promotions and other fun games that attract engagement. Using social media management systems like Hootsuite can also help with planning.

Don’t over post

Don’t add to the clutter by tweeting randomly 24 hours a day. Your audience will just tune it out. It’s more important to make fewer, more strategic posts, and to engage in a conversation. Do your research by looking at what people are discussing, find something relevant to your brand, and try to target a few smart tweets or posts into the discussion. Make sure to take the time to respond to your audience.

Use visuals

Evidence shows that the content that performs best on Twitter and Facebook includes visuals. In 2017, Cisco estimated that video in particular will represent 82 percent of all website traffic in 2021. That’s why it’s crucial that you look for any opportunities to include photos, videos or gifs in your posts. These are the kinds of posts that are likely to get more views, and more clicks.

Branch out but choose wisely

Considering the negative trends impacting the two juggernaut networks, it may be a good idea to branch out. If you’re not already utilizing Instagram, consider developing a marketing strategy that includes it. Instagram is growing in popularity because of its reliance on the visual. In general, it’s a good idea to go where your intended audience goes. But make sure to limit your marketing to no more than 3 networks, because trying to do everything at once can make it harder for you plan and execute the right strategy for each.

The bottom line

Don’t swear off Twitter and Facebook just yet. But understand that you may have a tougher time being noticed, so it’s doubly important to make sure that you understand your target audience, posting engaging content that appeals to this audience properly and reflects your brand. Don’t make the mistake of just posting content into a vacuum and hoping it will get noticed. Amid all the noise, give those quality users that are still there a good reason to engage with you and your brand.

Marketlend Academy survey: how important is marketing to you?

Businesses have different schools of thought on how much time and money should be devoted to marketing and which approaches are most suitable for their companies. We’d love to hear about yours. Please take a few minutes to respond to this brief survey. We’ll share our findings and hope they create some interesting conversations that foster our growing sense of community at Marketlend.

Take the survey now.

Listen To The Investor Townhall

This past week, Marketlend ran an investor townhall. Transparency is integral to how Marketlend operates. Our investors expect it and we are committed to delivering on this promise. The investor townhall offered a chance to roll up our sleeves and explore issues that matter to the investor community.

We dug down into the mechanics of how we return principal in the event of a problem loan and the integrity of the Marketlend platform generally. There was ample room for Marketlend’s Founder and CEO to field questions and the result was a really engaging and hopefully enlightening look inside the how and why of this aspect of the Marketlend platform. Click above to have a listen.

Marketlend Academy: 4 Signs Your Small Business Needs to Course Correct Now

So your launch was a success, and your new business is now at cruising altitude. Celebrate, by all means. But keep an eye out for tendrils of smoke in the vents.

That’s because some problems in a growing business are like a smouldering fire: you’re often unaware until it’s too late. If you know their early warning signs, though, and have plans in place to counteract them, you shouldn’t be taken by surprise. Here are some of those signs and the best countermeasures:

1. You’re starting to pay your bills late

If you’re starting to having trouble paying creditors and employees on time, you might be developing major cash-flow woes. Cash is everything to your small business, and you need to figure out where the problem lies right away.

Ask yourself: Are you billing your clients quickly enough, with timely invoices? Are you checking the credit histories of your big customers instead of just giving them the benefit of the doubt? What about collections procedures for the deadbeats? Do you have those in place?

Cut costs wherever you can. The little expenses add up. Barter with other businesses for services; buy your equipment gently used; install a ‘smart’ thermostat; get a solar water heater; make staff turn off computers at night; employ freelancers for suitable tasks. You can even borrow items from a tool library so you don’t have to buy them.

Check your financial statements religiously. Identify any possible opportunities to boost your income, but don’t even think about trying to grow right now. If you’re having cash flow problems, now’s not the time.

You should be able to pay your bills, your employees, and even yourself–on time.

2. You’re always reacting to emergencies

If you’re starting to respond to business emergencies day in, day out, something’s not right.Things should be running smoothly enough to let you plan and think strategically much of the time, and focus on building your business.

Perhaps you’re trying to have the business do too many things at once; or maybe you’re bad at setting priorities and managing time.

The Eisenhower Matrix

Have you heard of the Eisenhower Matrix? It’s a formula developed by Dwight Eisenhower, the American World War II general, more than 60 years ago that has stood the test of time. Basically, Eisenhower split his workload into urgent tasks (returning a phone call from Winston Churchill, say) ) and important tasks (such as planning for D-Day)). He made sure to schedule time for his important tasks and to delegate the unimportant ones. What he accomplished with this approach is none too shabby: he vanquished Hitler, became president of the U.S. and developed its highway system, among other things. And his formula is still alive today.

Eisenhower didn’t even have the benefit of project management apps, but you do. These can help you and your staff work together efficiently. Eisenhower also knew that having too many meetings in one’s schedule is a bad idea — they suck up lots of time.

Be realistic about your own weaknesses, and consider hiring someone to help set priorities and establish your office systems.

3. The staff you just hired is leaving

Once you’ve invested in training good people, you want them to stick around. If

they’re leaving sooner than you’d like, schedule exit interviews with them to ask why. Then ask yourself what you can do to improve staff retention.

And take a look in the mirror. A good boss fosters enthusiasm, sets clear expectations, gives timely feedback and conveys a sense of mission. Then he or she gives the employees room to get the job done. If they do their jobs well, don’t micromanage.

Let your employees know you value their efforts (or at least, let the good ones know); pay them a decent wage; express an interest in them. They’ll reward you with loyalty.

If these strengths aren’t yours, consider hiring someone else to manage your staff. Outside consultants can also help identify why employees keep heading for the door.

Turnover rates vary by industry, so you might want to call your industry’s trade association, if there is one, to see how your rate compares.

4. You experience a sudden drop in sales

A sudden drop in sales could be just a hiccup, but it could also be a sign of bigger problems, so investigate immediately. Have your competitors beat you to the punch in some way? Is your product or your way of selling it outdated? Do you need to adjust your pricing or your marketing? If you have sales staff, are they hitting their quotas?

Are you targeting the right customers? Is technology revolutionising your industry in some way and changing your customers’ buying habits or methods?

Put yourself in your customer’s shoes and try searching for your product and business online. If you sell online, make sure everything on your website functions smoothly, from landing to checkout.

Check in with your industry’s trade association, if you have one, to find out if the drop you’re experiencing is part of a bigger trend, or perhaps customary at this time of year for reasons you might not have thought of.

Now you have it — four situations, each of which could be a wisp of smoke telling you your engine’s on fire. Ignore them at your peril.

Marketlend Academy: Does your SME need a branding consultant?

Branding, where does it fit? Determining which job functions to prioritise in an SME is one of the most critical resource decisions you’ll make as a founder. The need to focus foremost on services and product development is obvious, but business experts often debate the merits of investing in strong branding.

It’s not necessarily a key factor in whether an investor may choose to fund your business, but it’s important to make a good impression. So how much money should you actually spend and who should you work with to build a reasonable branding plan? Consider some of the following factors to help you decide what’s best for your business.

What is your branding IQ?

If your idea of branding means paying a random designer $10 on Fiverr to create your logo, you might be underestimating some things. (That’s not to say this approach doesn’t magically work out well sometimes! Best of luck to you.) Get real with yourself about how much of a priority branding needs to be in your business. Plan to invest some time. In fact, let’s pause for a moment. Complete outsourcing is not really possible when it comes to branding. This business is your passion and even the best consultant will need you to set aside a few hours a week to collaborate and extract authentic representations of your work from you. The absolute worst thing you could do is throw money at someone and expect a brand to materialize without nurturing on your end.

How much can you expect out of your branding consultant?

At a bare minimum, a decent branding plan should involve 10-15 hours of work with a trusted professional who will create a roadmap for success. Advanced branding should be an integrated component of your overall marketing strategy. In the social media era, this usually includes a supplemental content strategy for which you would create assets like written blog content, graphics, photos, podcasts or videos. You’d also want to create a system for deploying this branded content to firmly-defined key audiences. A top-notch branding consultant should be able to help you conceptualize your aesthetic, your content and deployment strategy, and connect these efforts back to your sales funnel.

Where can you find them?

As you begin your search, consider the merits of working with an agency versus a freelance individual. Intangibles, such as personal compatibility and working styles, are also important. Agencies offer more brain power and hands on deck; the access to a broader infrastructure can lead to increased operational smoothness and responsiveness.They are also more expensive than individuals, who often leave agencies to enjoy the benefits of self-employment. Be open-minded. Branding consultants are usually creatives who embrace flexibility. Just be wary of anyone who presents themselves as a one-stop shop of expertise. Ask an individual who else they plan to work with on design and production, and find out if there are hidden or unanticipated costs for ancillary things like social media advertising budget on top of their fees.

The best bet is to ask colleagues for recommendations. You can also try LinkedIn searches. Sites like CloudPeeps, Dribbble, Carbonmade, and Thumbtack can also be a good bet. You may also want to research private Facebook groups for freelance creative professionals and see if you can post your job description.

How much should you invest?

Your budget will be a major factor in how things go with your branding consultant.

There are awesome, enterprising young people who are building up their portfolios willing to work for as low as $25-50/hour. A mid-career professional can run about $75/hour. Heavy-hitters will ask for $150+ hourly rates. Any of these folks might be willing to negotiate a flat rate deal with you as well. Agencies typically charge a monthly retainer from $2,500 to $10,000. Be willing to suggest a startup discount, services trade, or payment installment plan if it would allow you to work with someone you’re excited about. They might say yes!

How long should you work together?

The duration of your agreement is heavily dependent on your initial goals. A top-level evaluation from a major strategist could take a week. A first iteration and basic roadmap could be completed in 4-6 weeks. A more advanced engagement could last 3-6 months. Whatever you decide in coordination with your branding consultant, be sure to build a mid-point check in to ensure you’re on track to hit your agreed upon deliverables.

Marketlend Academy: Marketing Your SME

Let’s say you’ve come up with a cure for baldness. You’ve patented your formula, written a business plan, lined up investors, hired staff and set up production. Ready for liftoff, right? Nope. Your startup would crash for want of marketing.

You can’t sell something, even the cure for baldness, unless people know it exists. Lots of people. Marketing is how you let them know your product exists, and also how you make it appealing. Product design, consumer research and advertising all come under marketing’s umbrella. Pricing strategy–or at least, the case you make to the consumer that the price is right–comes under marketing, too.

The elements are many, and your business needs an approach that incorporates some or all of them. The best strategy for any given business usually includes a mix. For example, logo development, media outreach, paid advertising and trade shows. Here are tips for deciding what marketing strategies might work for your startup and ways to get started.

Fine-tune your marketing plan

Ideally, your business plan addressed marketing to some degree, but you’ll want to flesh this out in a plan exclusively focused on marketing before you go live. You’ll want it to start with an explanation of why your product is better than your competitors’ and accurately describe your niche.This is called the “situational analysis.”

Add on a short description of your ideal prospective customer and their earnings, gender, age, family composition and consumer habits. Also Include the type of media this hypothetical person likes to consume–internet, newspapers, television, radio, podcasts, etc.. A person over 65, for example, is less likely to use Instagram than a person in their early 20s. This section will require you to do a bit of research, but it will bear fruit.

Next, list some very specific, measurable goals you want to reach, such as a 10 percent increase in sales in your second year of operations. You want your goals to be measurable so you’ll know if you reached them.

And of course, you need to list your tactics for spreading the word about your product so that it reaches prospective customers. Take into account the different stage of the sales cycle and determine how you plan to reach cold prospects and how you want to reach existing customers, whether its through radio advertising or loyalty programs. Options are many, from banner ads online to banners pulled by planes; from chatty blogs to the sparse wording on a billboard.

Set your marketing budget

Be prepared: marketing can be costly. Most startups decide on a marketing budget that’s a percentage of their projected revenue. But the recommended ratio varies by industry, so it would be wise to seek advice from your industry’s trade association.

Some companies spend up to half of their sales revenue on marketing in their first year and 30 percent of that revenue thereafter. One school of thought holds that companies in their first five years of business should allocate 12 to 20 percent of their gross or projected revenue for marketing every year while older companies should allocate up to 10 percent. One tool that might be helpful is the National Australia Bank’s marketing budget forecast template.

Measure your results

Unless you measure the results of your marketing efforts, it’s hardly worth drawing up a plan in the first place. Measurement helps you fine-tune your tactics so they’re better at reaching your intended audience. It lets you know when an approach isn’t working so you can regroup and try something else. Your metrics will hinge on your tactics. Print advertising could direct people to a designated phone number or internet domain and you could count how many calls or views it gets. Online promotions and clicks can be measured using internet analytics. If you use billboard advertising, the billboard company will have a way to measure the number of cars and pedestrians who walk past every day.

Planning backed up by careful research; budgeting that’s realistic; and measuring that tracks results are cornerstones of effective marketing. If you market your product well, potential customers will recognize your brand, distinguish it from your competitors and favor it.

Marketlend Passes The $50 Million Mark

$50 million! It’s time to take a moment to celebrate. Marketlend is pleased to announce that we have hit $50 million lent through our first-of-its-kind platform.

Our strong investor community and our strong SME community is a major reason for reaching this milestone. We want to express our thanks to you for helping us make this happen, and supporting us as we grow into the future.

We’re not celebrating for long, though, because there is a lot of ongoing work to do. We continue to develop better risk assessment methods, a richer tool set for our investors and more ways to support our entire community, including new lending channels and opportunities (soon to be announced!).

In other news, take a listen to Marketlend’s Founder and CEO, Leo Tyndall, talk to Alan Kohler on Qantas Business Radio here.

Marketlend Academy: Hiring an IT Consultant for your SME

Hiring an outside IT consultant is often fraught with anxiety for companies and their IT managers. Regardless of how well-regarded the consultant is, he or she is still accessing a company’s secure environment and encroaching on the IT department’s turf.

Reasons for management nail-biting abound. IT consultants are often authorized to do things with the system that the regular IT employees aren’t allowed to do. The consultants are typically tied in with a services contract – meaning they get paid no matter what happens. Consultants are there to do only what they’ve been contracted for, even if IT management disagrees with what they’re doing or how they’re doing it. Consultants also tend to cost a lot of money.

Perhaps most frustrating for IT managers is that the department could probably do the job themselves – if they were only given the proper resources.

Why hire an IT consultant?

For all the worry IT consultants may cause, they can be a key factor in improving a company’s information technology processes, spotting potential security risks or helping to retrain and recharge the department.

The consultants’ biggest strength is that they bring a knowledgeable outsider’s view to a company’s technology problems. For IT departments bogged down in the day-to-day challenge of keeping a network running and servicing users throughout the buildings (or handling IT in multiple buildings across the country or worldwide), it can be difficult to keep a broader, strategic perspective on things.

The right consultant can be a breath of fresh air for an enterprise that is looking for better, cost-effective ways to manage complex IT issues.

Still, companies need to make sure that an IT consultant has precisely the right skills for the project that they have in mind. They also need to make sure the consultant stays on task and works smoothly with the existing IT team.

Where Kablamo fits in

One big issue companies may have with IT consulting firms is that the consultant may blur the lines between purely providing a service versus controlling or fundamentally changing the client’s way of doing things.

A consultant should take the time to really listen to a client’s needs and understand the challenges they want to overcome. He or she should be ready to dig in to discover the best possible solutions. These attributes help to prevent a disconnect between the client’s expectations and the outcome, as Kablamo’s co-CEO Angus Dorney explains.

The rise of enterprise cloud services has amplified worries about consultants’ role with an enterprise. Ditto with the increasing popularity of artificial intelligence (AI) and machine learning technologies. Now, companies looking to shift into cloud, or to add an AI element to their network – a technology segment still in its infancy – must contend with finding a consultant that understands what is needed to complete the shift. When it comes to cloud services, consultants need to provide a more complete package – a strategic overview of what’s needed, along with the experience and skills to implement the shift to enterprise cloud. Figuratively speaking, a consultant cannot merely provide apples when what an enterprise needs is an apple pie.

What to look for

Say a company needs to evaluate the value of putting a majority of its IT assets into a cloud environment. The IT department may have employees who are able to handle some of this evaluation but may not be able to reassign those employees to perform an in-depth study of the company’s needs. They may not have all the resources necessary to do a proper assessment, either.

This is typically where management calls in a consultant. Knowing what to look for in a consultant is crucial to completing an accurate assessment that will help the company decide how much of its IT infrastructure to shift into a managed cloud environment.

Key questions to ask:

- What expertise does the consultant have? Does that expertise fit within a specific industry niche or within a broader strategic overview?

- How will the consultant work with a company’s IT team? Will the process be collaborative, with meaningful input from employees and stakeholders?

- Is the consultant familiar with the regulations and/or IT practices and policies of the company? What about government compliance requirements, if any?

- Does the consultant really listen to the stakeholders to try and understand exactly what the company is trying to overcome by bringing them in?

Tips for getting the most out of an IT consultant

- Have goals in mind before hunting for a consultant – you don’t need to have all of them, but some direction should be provided.

- Put together as much information about your company as possible to give to the consultant before they begin.

- Direct relevant departments to partner with the consultant so that effective collaboration or assistance take place. (For example, if a consultant needs to do a security gap analysis, make sure the IT department is ready and able to give him or her access to key systems.)

- Look at hiring a consultant as an investment, not as a luxury or as a necessary evil.

Empowering the IT department

A company should look at the IT department, or at the very least its management, as key stakeholders in any strategy or project developed by consultants. At the end of the day, the IT department must deal with whatever technology improvements and processes are put into place by a consultant.

Shifting into a cloud-native architecture, for example, can be a massive and potentially stressful undertaking by IT department employees – even more so if the consultant and employees aren’t working together to move a project forward. Relying entirely upon outside labor to complete the shift can generate some resentment within the department, particularly from employees who feel they’re capable of doing the job if given the right resources or simply the ability to give feedback on a proposal or project.

Companies need to look at the IT department as a key resource and partner for the consultant. Employees’ in-depth knowledge of a company’s technology needs and processes is very important to ensure a comprehensive plan of action is created. Otherwise, the risk of an unsatisfactory outcome, or even a compromised network, is a possibility.

Tips:

- Make IT department managers or IT executives key stakeholders on consultant-driven projects.

- Ensure open lines of communication between consultants and IT employees so they understand the consultants’ role.

- Give the IT department time to respond to proposed changes to the enterprise network, and to give feedback throughout the consultant’s study or proposed work.